Please find our most recent market review below. We hope these perspectives are valuable to you.

– The AdvicePeriod Team

Key observations

- Global growth remained positive but slowed, with S&P Global cutting its 2026 GDP forecast to around 2.2% and U.S. Q1 real GDP running near a 2.0% annualized pace. The overall narrative in May shifted from “reacceleration” to “moderate expansion with rising downside risks.”

- Inflation progress stalled as elevated oil and commodity prices kept price pressures sticky, especially in Europe and parts of Asia. This reinforced expectations that central banks, including the Fed, would keep policy rates higher for longer with only limited cuts in 2026.

- Equity markets, led by U.S. technology and artificial intelligence (AI)-related names, hovered near record highs even as valuations looked stretched and gains were narrow. Meanwhile, consumer confidence softened and bond yields moved up, highlighting a growing gap between upbeat markets and more cautious households and fixed-income investors.

Global markets in May were defined by steady but slower economic growth, sticky inflation and interest rates, and equity markets that continued to advance despite lingering macro and geopolitical risks. What follows is a review of the key developments over the month and how they shaped the broader investment landscape.

Economic growth: Slower but still positive

The global economy in May 2026 remained in expansion, but at a more modest pace than earlier in the year, with estimates for 2026 growth marked down to around 2.2% from roughly 2.9% as higher energy costs and tighter financial conditions weighed on activity. In the United States, real GDP grew at about a 2.0% annualized rate in the first quarter, pointing to an environment best characterized as “moderate growth” rather than boom or recession, with the economy still resilient but clearly cooling.

This combination of slower global growth alongside a still-expanding U.S. reinforced a soft-landing narrative rather than signaling an imminent global downturn. For investors, May’s backdrop remained one in which economic activity continues to support corporate earnings, even if the underlying growth impulse is less robust than in earlier stages of the cycle.

Inflation and interest rates: pressures remain

Inflation pressures in May remained persistent, especially through the energy channel, with disruptions in the Middle East and heightened tensions around the Strait of Hormuz keeping oil prices volatile and slowing the decline in headline inflation. Across regions, inflation in several advanced economies stayed above central bank targets, with energy and services prices continuing to play a significant role, and global projections suggested that inflation is likely to edge up in 2026 before gradually easing into 2027.

In this environment, expectations for interest rates shifted further toward a “higher for longer” path, as multiple central banks either kept policy firmly in restrictive territory or implemented additional rate increases. For the United States and other major economies, the prevailing outlook in May was one where moderate growth and unemployment rates in the mid‑4% range coexist with tight monetary policy, implying that the peak in inflation is likely behind but the journey back to target will be drawn out rather than rapid.

Markets: Equity strength amid crosscurrents

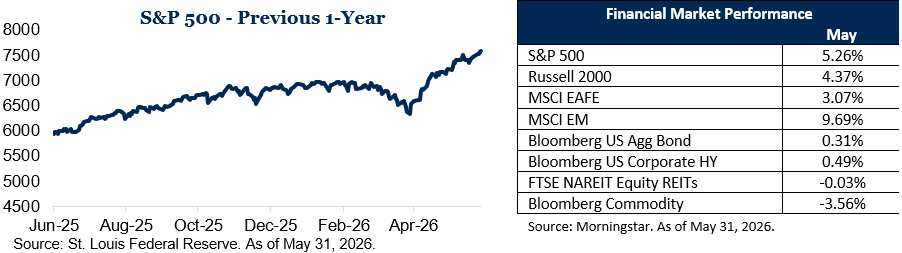

Financial markets in May processed the combination of slower growth and persistent inflation in a way that continued to favor risk assets, particularly equities. Global equity indices reached or approached new all-time highs after a strong April, leaving stocks near record territory even as the macro backdrop remained mixed.

Leadership was still concentrated in U.S. markets and sectors linked to technology and artificial intelligence, where enthusiasm around productivity gains and earnings growth remained a key driver of performance. This concentration meant that, despite strong headline index levels, underlying market breadth was more uneven, with many areas lagging the largest growth and AI-related names.

Fixed income markets told a different story, as investors reassessed the timing and extent of future rate cuts and pushed sovereign yields higher. For diversified portfolios, this created a familiar tension between buoyant equity returns and renewed pressure on bond prices as yields adjusted to a “higher for longer” policy and inflation outlook.

Sentiment and confidence: Cautious beneath the surface

Major equity indices continued to trade near record levels in May, but sentiment data showed consumers taking a more cautious view of conditions. The US Consumer Confidence Index edged lower, with respondents reporting softer assessments of current business conditions and the labor market.

This dip in confidence occurred alongside an ongoing stock market rally and still-strong labor headlines, highlighting a divergence between financial market performance and household perceptions. At the same time, geopolitical tensions and the risk of energy-related shocks remained important sources of macro uncertainty, reinforcing a sense of unease beneath the surface of headline asset prices.

Such divergences are common late in economic cycles, and May’s data fit that pattern: asset prices reflected optimism about earnings and innovation, while consumers and policymakers stayed sensitive to inflation, borrowing costs and geopolitical risks. The result was an environment that remained supportive in many respects but also complex, with constructive and challenging forces coexisting rather than pointing in a single clear direction.

Thank you for taking the time to review this month’s update. May 2026 underscored that markets can continue to make progress even as growth moderates, inflation pressures linger and confidence remains uneven, with equities still drawing support from solid economic activity and ongoing enthusiasm for large‑cap technology and AI‑related leaders.

At the same time, elevated energy prices, higher bond yields, and a slower path toward lower policy rates remain key features of today’s landscape, and the environment continues to be constructive but defined by meaningful crosscurrents that we will monitor closely on your behalf.

This market commentary is meant for informational and educational purposes only and does not consider any individual personal considerations. As such, the information contained herein is not intended to be personal investment advice or a recommendation of any kind. The commentary represents an assessment of the market environment through May 2026.

The views and opinions expressed may change based on the market or other conditions. The forward-looking statements are based on certain assumptions, but there can be no assurance that forward-looking statements will materialize.

Equity securities are subject to price fluctuation and investments made in small and mid-cap companies generally involve a higher degree of risk and volatility than investments in large-cap companies. International securities are generally subject to increased risks, including currency fluctuations and social, economic, and political uncertainties, which could increase volatility. These risks are magnified in emerging markets.

Fixed-income securities are subject to loss of principal during periods of rising interest rates and are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications, and other factors before investing. Interest rates and bond prices tend to move in opposite directions. When interest rates fall, bond prices typically rise, and conversely, when interest rates rise, bond prices typically fall.

There is no assurance that any investment, plan, or strategy will be successful. Investing involves risk, including the possible loss of principal. Past performance does not guarantee future results, and nothing herein should be interpreted as an indication of future performance. Please consult your financial professional before making any investment or financial decisions.

AdvicePeriod is another business name and brand utilized by both Mariner, LLC and Mariner Platform Solutions, LLC, each of which is an SEC registered investment adviser. Registration of an investment adviser does not imply a certain level of skill or training. For additional information about Mariner, LLC or Mariner Platform Solutions, LLC, including fees and services, please contact us utilizing the contact information provided herein or refer to the Investment Adviser Public Disclosure website (www.adviserinfo.sec.gov).

For additional information as to which entity your adviser is registered as an investment adviser representative, please refer to the Investment Adviser Public Disclosure website (www.adviserinfo.sec.gov) or the Form ADV 2B provided to you. Investment adviser representatives of Mariner, LLC are generally employees. Investment adviser representatives of Mariner Platform Solutions, LLC dba AdvicePeriod, are independent contractors.

Indexes referenced are unmanaged and cannot be directly invested into. For index definitions visit https://www.marinerwealthadvisors.com/index-definitions/.

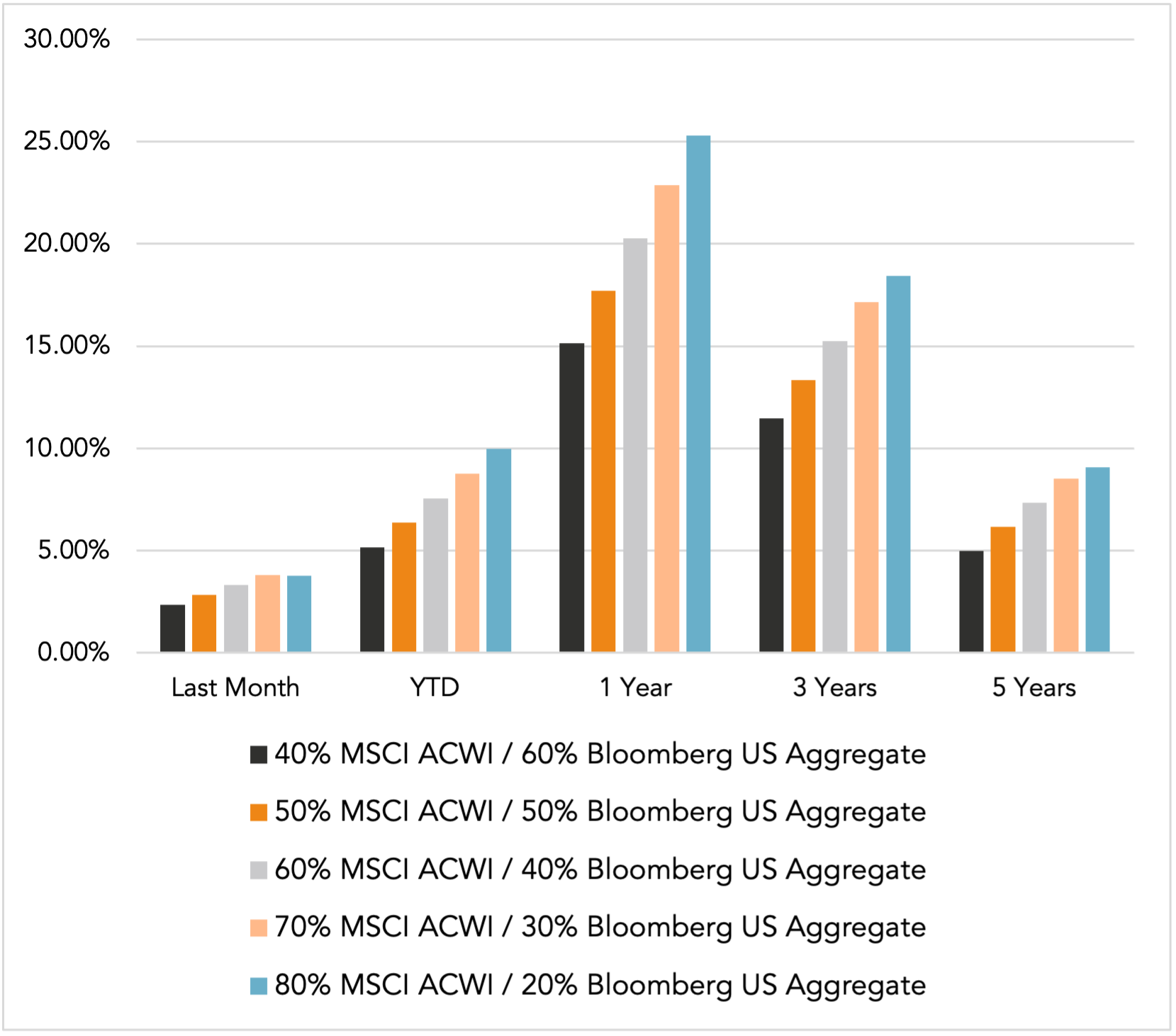

Does past performance matter?

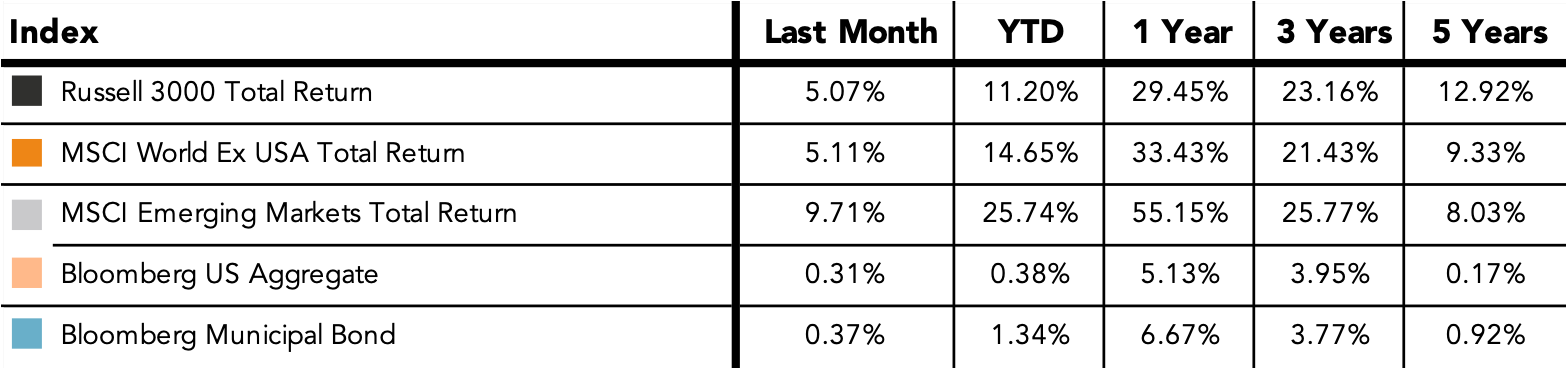

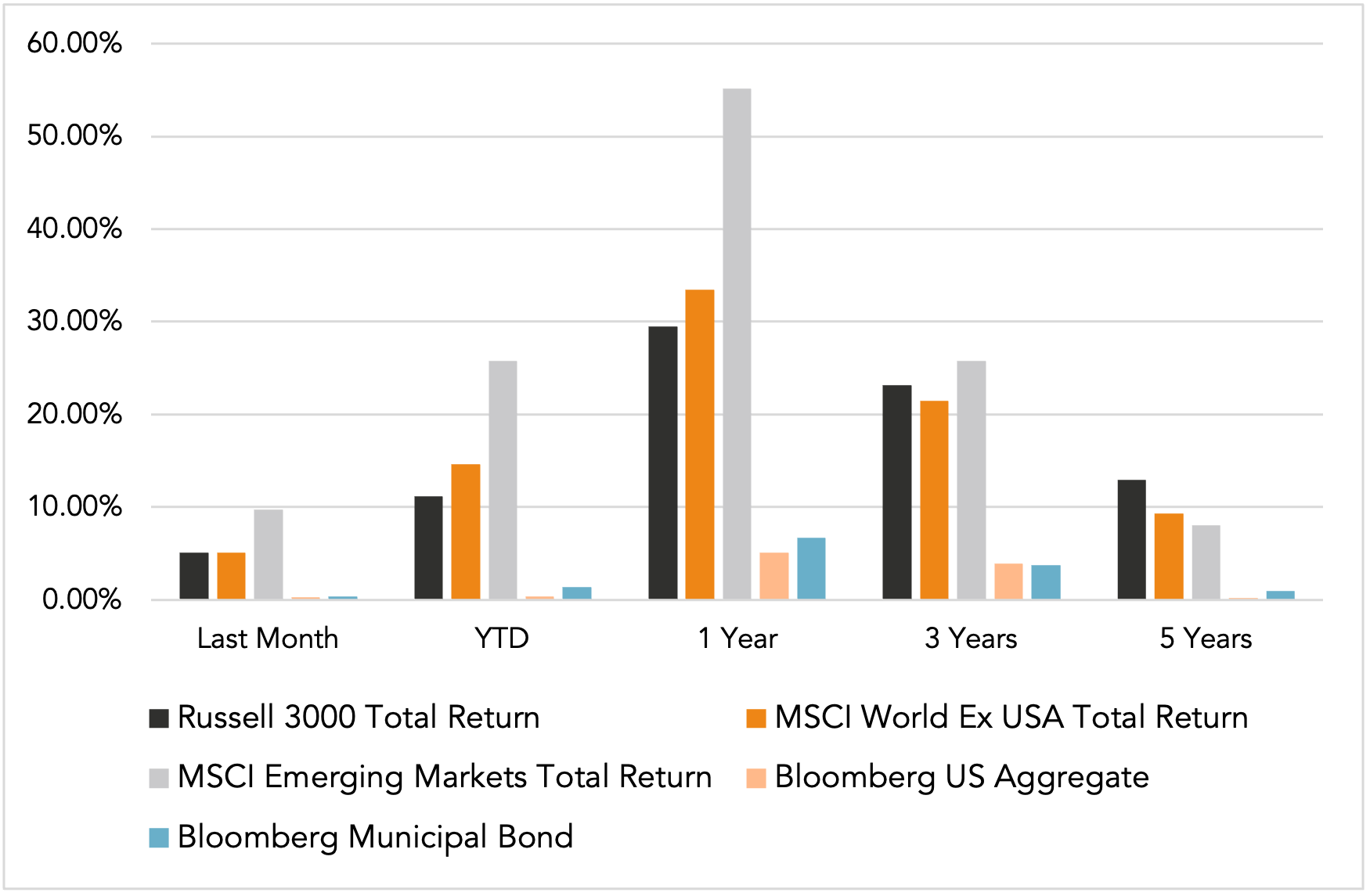

Major Market Index Returns

Period Ending 5/1/2026

Multi-year returns are annualized.

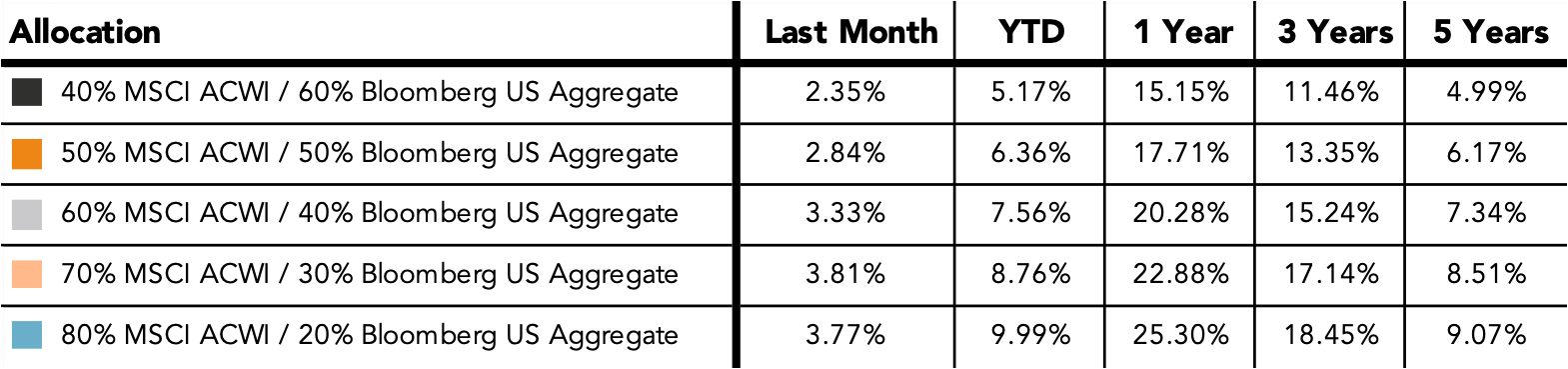

Mix Index Returns

Global Equity / US Taxable Bonds

Indexes are unmanaged and cannot be directly invested into. Past performance is no indication of future results. Investing involves risk and the potential to lose principal.

The Russell 3000 Index is a United States market index that tracks the 3000 largest companies. MSCI Emerging Markets Index is a broad market cap-weighted Index showing the performance of equities across 23 emerging market countries defined as emerging markets by MSCI. MSCI ACWI ex-U.S. Index is a free-float adjusted market capitalization-weighted index that is designed to measure the equity market performance of developed and emerging markets excluding companies based in the United States. Bloomberg U.S. Aggregate Bond Index represents the investment-grade, U.S. dollar-denominated, fixed-rate taxable bond market, including Treasuries, government-related and corporate securities, as well as mortgage and asset-backed securities. Bloomberg Municipal Index is the US Municipal Index that covers the US dollar-denominated long-term tax-exempt bond market. The index has four main sectors: state and local general obligation bonds, revenue bonds, insured bonds, and prerefunded bonds.

Monthly Market Update – June 2026