Please find our most recent market review below. We hope these perspectives are valuable to you.

– The AdvicePeriod Team

Key observations

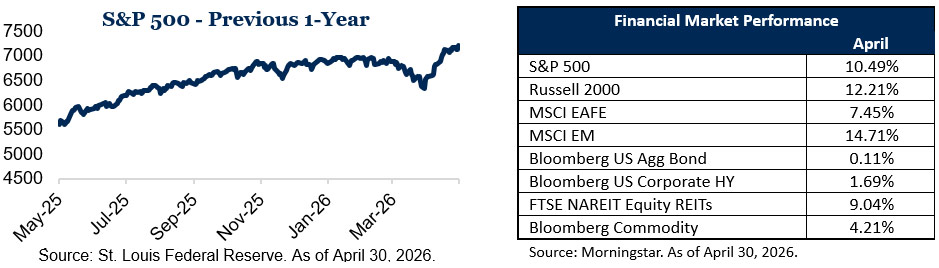

- Global equities rallied strongly in April, with major indices like the S&P 500 and Nasdaq back at or near record highs, led by artificial intelligence (AI)‑ and tech‑related names. Market leadership remains tech‑heavy but has started to broaden toward mid‑ and small‑cap stocks.

- Oil prices jumped on renewed Middle East tensions and shipping disruptions, pushing Brent above 110 dollars and adding fresh pressure to headline inflation. Even so, forecasts still see U.S. and global growth roughly around trend, supported by corporate earnings and AI‑driven investment.

- Major central banks, especially the Fed, stayed on hold and signaled less urgency to cut as inflation has proven stickier than hoped. Markets have scaled back expectations for 2026 rate cuts, and bond yields have risen even as credit spreads remain relatively tight.

April 2026 was a busy month across global financial markets. Equity indices moved higher, oil prices rose sharply amid renewed geopolitical tensions, and central banks—most notably the U.S. Federal Reserve—maintained a cautious stance as they weighed mixed inflation data against still‑resilient growth.

Equity markets: Strong month across major indices

U.S. equities delivered robust gains in April, with the S&P 500 setting new record highs. The index reached those highs after gaining roughly 10.5% over the prior month and nearly 30% versus the same time a year earlier. These advances followed a weaker first quarter, with the index down about 4.35% year to date at the end of March, highlighting the rebound in sentiment as April progressed.

The leadership behind these gains remained concentrated in large technology and AI‑linked companies. At the same time, equal‑weight indices and mid‑ and small‑cap segments showed improved relative performance compared with earlier in the year, indicating somewhat broader participation even though mega‑cap growth stocks continued to lead overall.

Corporate fundamentals provided a supportive backdrop. By the end of the month, about 63% of S&P 500 companies had reported first‑quarter results, and 84% of these firms reported earnings above consensus expectations, with both the frequency and size of upside surprises running above recent averages. The index was on track for a sixth consecutive quarter of double‑digit year‑over‑year earnings growth, underscoring the continued strength of aggregate profits.

Outside the United States, many developed and emerging equity markets also rose in April. Markets in Europe and Asia advanced alongside the U.S., with notable strength in countries tied to technology supply chains and exporters, even as some regions faced the headwind of higher energy prices. Overall, April added to the longer‑running equity uptrend but also left valuations higher than earlier in the year.

Energy markets and inflation: Oil shock, but growth still steady

Energy markets were a key driver of macroeconomic developments in April. Geopolitical tensions in the Middle East, including concerns about the Strait of Hormuz, pushed Brent crude to its highest levels in four years. By the final days of April, Brent was trading in the 111 to 118 dollar range in several sessions, while U.S. benchmark WTI hovered in the low‑100s, leaving both measures significantly higher than at the start of the year.

These energy price moves fed directly into inflation readings and forecasts. The International Monetary Fund (IMF)’s April 2026 World Economic Outlook projected that the renewed oil shock would push global headline inflation somewhat higher in the near term, even as underlying or core inflation continued to gradually ease in many economies. In the U.S., data going into the April Federal Reserve meeting showed firmer CPI readings, with energy costs responsible for a substantial share of the recent pickup; energy prices were rising at double‑digit annual rates in the March inflation report, led by gasoline and fuel oil.

Despite the inflation impact, major institutions continued to project that global growth would remain near its long‑run trend rather than fall into recession. The IMF’s April projections described a global economy expanding at a moderate pace, with some downgrades for energy‑importing regions but continued support from business investment, including technology and AI‑related capital spending. U.S.‑focused outlooks pointed to a still‑resilient labor market and solid corporate balance sheets as factors that help offset the drag from higher energy costs and past rate increases.

The combination of higher headline inflation and relatively stable growth kept attention on the potential persistence of the energy shock. Economic research published in mid‑April noted that a prolonged period of elevated oil prices could increase the risk of second‑round effects on wages and non‑energy prices, potentially complicating efforts to return inflation to 2% targets. For the moment, many central banks are treating the spike as a negative supply shock that can be accommodated within limits as long as core inflation remains on a gradual downward path.

Central banks and interest rates: On hold, with a cautious tone

In this environment, the U.S. Federal Reserve left its benchmark interest rate unchanged at its April meeting. On April 29, the Federal Open Market Committee maintained the federal‑funds target range at 3.5% to 3.75%, in line with market expectations. The statement accompanying the decision described inflation as “elevated,” cited the recent increase in global energy prices, and emphasized that future decisions would remain data‑dependent.

The April decision featured an unusually high level of internal dissent. Four committee members voted against the decision—the highest number of dissents at a single meeting since the early 1990s—highlighting differing views on how to weigh resurgent inflation pressures against ongoing economic resilience. While the Fed retained language indicating that rate cuts are still possible over time, several officials in recent weeks have suggested that inflation risks could justify keeping rates at current levels for longer than previously anticipated.

Market expectations adjusted in response to the data and the Fed’s stance. Earlier in the year, futures markets had implied a series of Fed cuts in 2026, but by late April investors were pricing in fewer cuts and a later start to any easing cycle. In other developed economies, central banks have also largely paused rate changes and signaled that the path toward lower policy rates is likely to be slower and more uncertain than earlier forecasts suggested.

Fixed income markets reflected this shift. Government bond yields moved higher in April, particularly at intermediate maturities, as investors demanded additional compensation for inflation and fiscal risks. Credit spreads on investment‑grade corporate bonds remained relatively tight, supported by strong early‑season earnings data and ongoing investor risk appetite.

Putting April in context

Taken together, April 2026 was marked by strong equity performance, an energy‑driven rise in headline inflation and central banks that are firmly in “wait‑and‑see” mode. U.S. stocks, especially large‑cap and technology‑oriented names, pushed major indices to new highs, supported by ongoing earnings strength. Oil prices, influenced by geopolitical developments in the Middle East and concerns about supply through key shipping lanes, added complexity to the inflation outlook.

For policymakers, the main challenge remains balancing price stability and growth. As of the end of April, baseline forecasts from major institutions point to a global economy that is more likely to slow gradually than to contract sharply, although risks around this baseline—especially those linked to energy markets and geopolitics—have increased. In this setting, financial markets may continue to react sensitively to incoming data on inflation, growth and corporate earnings as investors reassess how long current interest‑rate and profit conditions can persist.

We will continue to monitor these developments and keep you informed through our regular updates.

This market commentary is meant for informational and educational purposes only and does not consider any individual personal considerations. As such, the information contained herein is not intended to be personal investment advice or a recommendation of any kind. The commentary represents an assessment of the market environment through April 2026.

The views and opinions expressed may change based on the market or other conditions. The forward-looking statements are based on certain assumptions, but there can be no assurance that forward-looking statements will materialize.

Equity securities are subject to price fluctuation and investments made in small and mid-cap companies generally involve a higher degree of risk and volatility than investments in large-cap companies. International securities are generally subject to increased risks, including currency fluctuations and social, economic, and political uncertainties, which could increase volatility. These risks are magnified in emerging markets.

Fixed-income securities are subject to loss of principal during periods of rising interest rates and are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications, and other factors. Interest rates and bond prices tend to move in opposite directions. When interest rates fall, bond prices typically rise, and conversely, when interest rates rise, bond prices typically fall.

There is no assurance that any investment, plan, or strategy will be successful. Investing involves risk, including the possible loss of principal. Past performance does not guarantee future results, and nothing herein should be interpreted as an indication of future performance. Please consult your financial professional before making any investment or financial decisions.

AdvicePeriod is another business name and brand utilized by both Mariner, LLC and Mariner Platform Solutions, LLC, each of which is an SEC registered investment adviser. Registration of an investment adviser does not imply a certain level of skill or training. For additional information about Mariner, LLC or Mariner Platform Solutions, LLC, including fees and services, please contact us utilizing the contact information provided herein or refer to the Investment Adviser Public Disclosure website (www.adviserinfo.sec.gov).

For additional information as to which entity your adviser is registered as an investment adviser representative, please refer to the Investment Adviser Public Disclosure website (www.adviserinfo.sec.gov) or the Form ADV 2B provided to you. Investment adviser representatives of Mariner, LLC are generally employees. Investment adviser representatives of Mariner Platform Solutions, LLC dba AdvicePeriod, are independent contractors.

Indexes referenced are unmanaged and cannot be directly invested into. For index definitions visit https://www.marinerwealthadvisors.com/index-definitions/.

Does past performance matter?

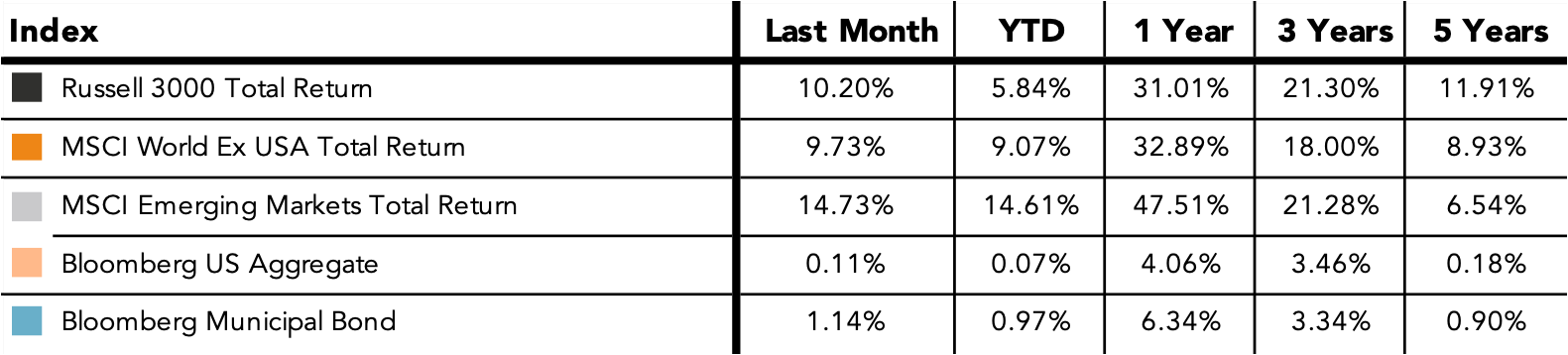

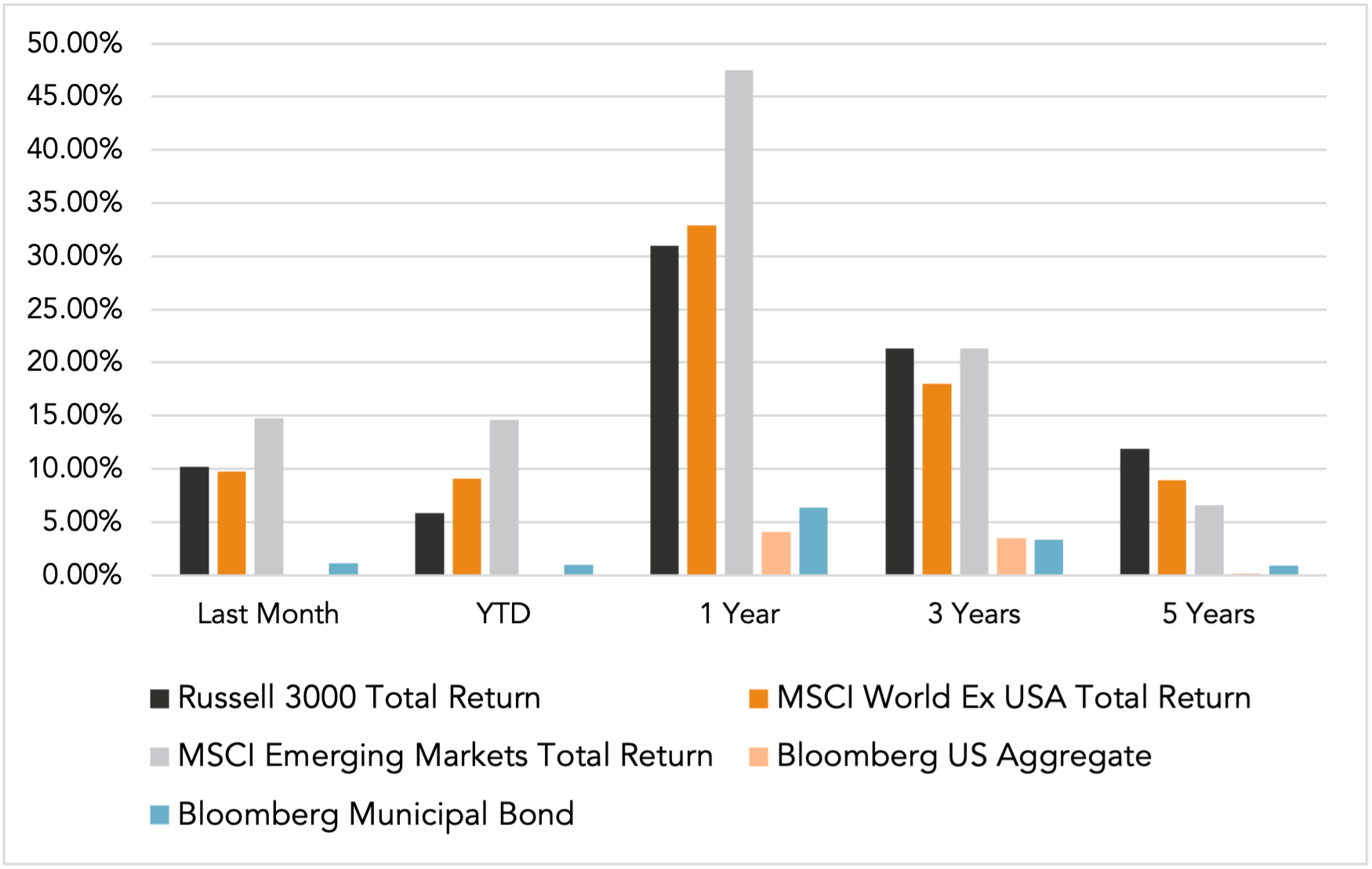

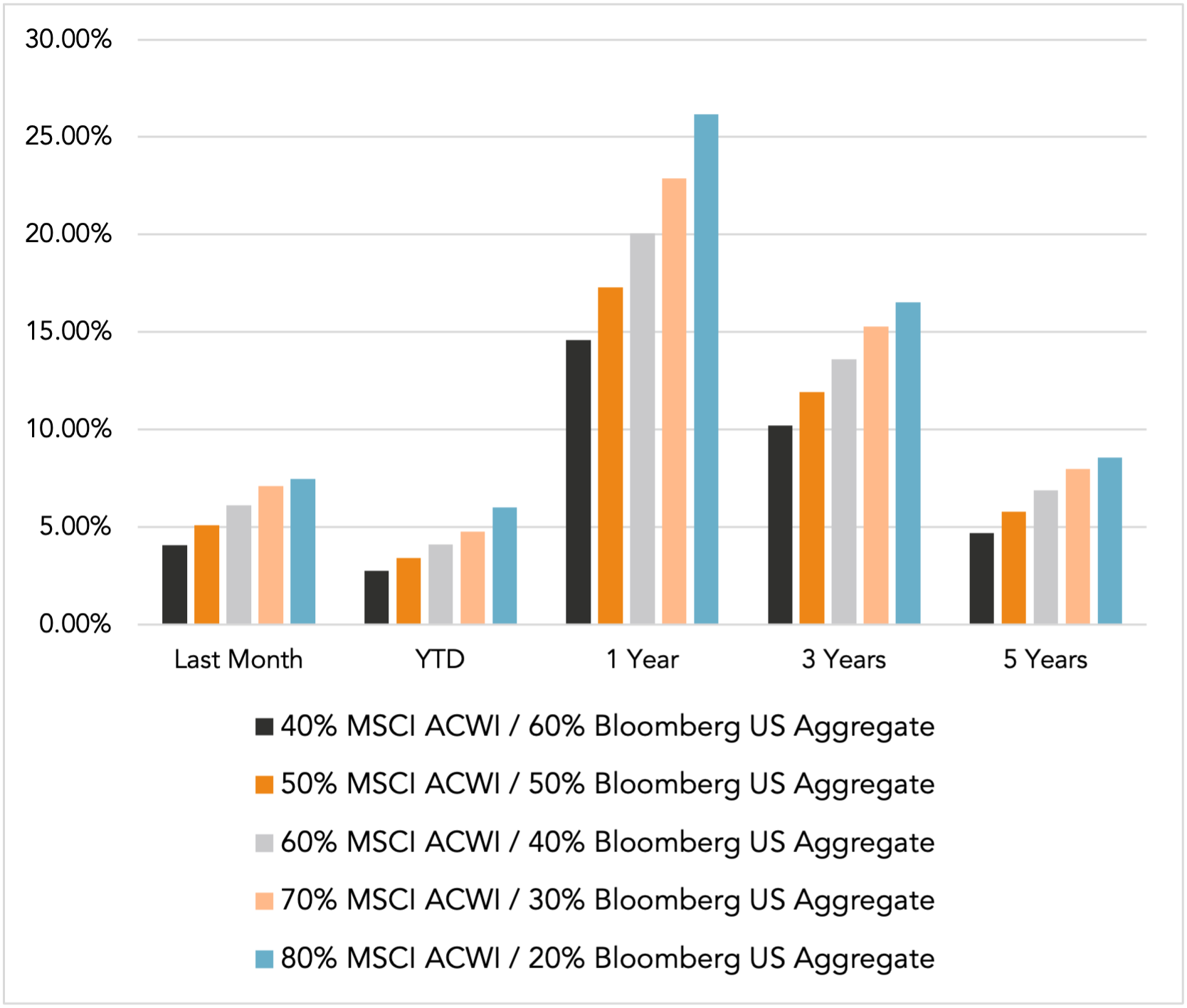

Major Market Index Returns

Period Ending 4/1/2026

Multi-year returns are annualized.

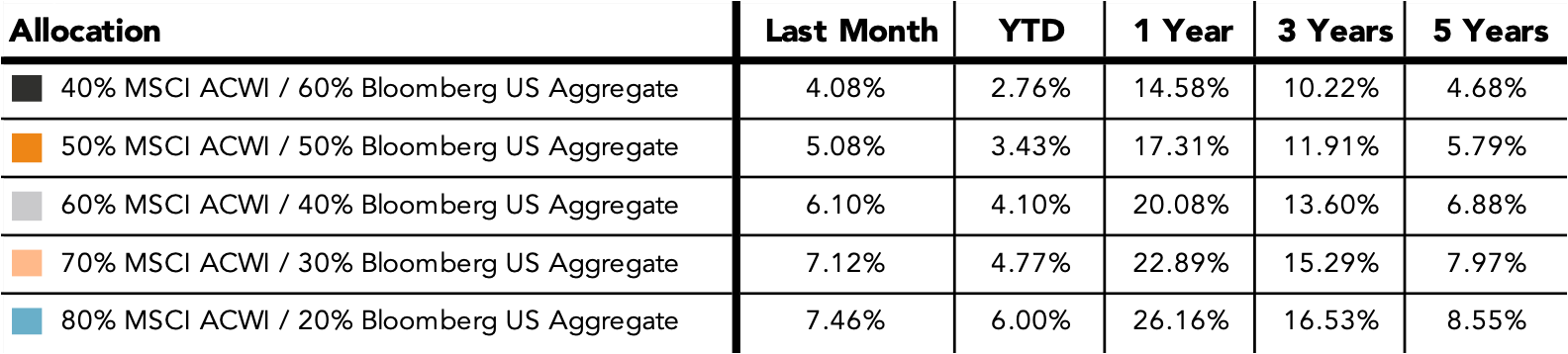

Mix Index Returns

Global Equity / US Taxable Bonds

Indexes are unmanaged and cannot be directly invested into. Past performance is no indication of future results. Investing involves risk and the potential to lose principal.

The Russell 3000 Index is a United States market index that tracks the 3000 largest companies. MSCI Emerging Markets Index is a broad market cap-weighted Index showing the performance of equities across 23 emerging market countries defined as emerging markets by MSCI. MSCI ACWI ex-U.S. Index is a free-float adjusted market capitalization-weighted index that is designed to measure the equity market performance of developed and emerging markets excluding companies based in the United States. Bloomberg U.S. Aggregate Bond Index represents the investment-grade, U.S. dollar-denominated, fixed-rate taxable bond market, including Treasuries, government-related and corporate securities, as well as mortgage and asset-backed securities. Bloomberg Municipal Index is the US Municipal Index that covers the US dollar-denominated long-term tax-exempt bond market. The index has four main sectors: state and local general obligation bonds, revenue bonds, insured bonds, and prerefunded bonds.

Monthly Market Update – June 2026