Please find our most recent market review below. We hope these perspectives are valuable to you.

– The AdvicePeriod Team

Key observations

- The U.S. and global economies remained more resilient than expected in the first half of 2026, despite tighter financial conditions and geopolitical shocks. Growth has started to cool at the margins, with advanced economies slowing modestly while some emerging markets benefit from trade and commodity tailwinds.

- Inflation continued to ease from prior peaks but stayed above central bank targets, keeping the “sticky inflation” narrative intact. This has left major central banks in a cautious “wait-and-see” stance on rate cuts, balancing the risk of rekindling inflation against the drag from higher rates.

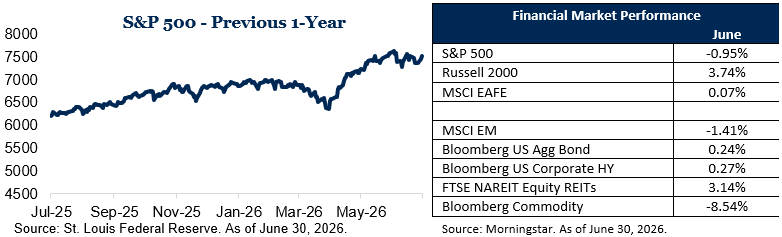

- Equity gains broadened meaningfully beyond U.S. mega-cap technology stocks, as investors moved further out on the risk spectrum amid easing recession fears and improving earnings expectations. Small caps were up 22.7% and emerging markets 24% through June 30, signaling meaningful catch-up and expanded leadership beyond prior years’ narrow large-cap growth winners.

June marked an important milestone for markets and the economy, closing out the first half of 2026. The month featured resilient economic data, persistent inflation pressures and a notable broadening of equity market leadership beyond the narrow group of mega-cap technology stocks that had dominated in recent years.

Growth resilient but moderating

Global data in June portray an economy that is slowing from its post-pandemic rebound but still expanding. The United Nations’ Department of Economic and Social Affairs placed the 2026 global growth forecast at 2.5%, which would be the weakest pace of expansion outside of a formal recession in nearly two decades and reflects the impact of higher energy prices, geopolitical uncertainty and tighter financial conditions. Even with this weaker outlook, the overall picture remains one of continued, modest growth rather than contraction.

In the United States, growth and employment trends remained firm into midyear. A June snapshot of the labor market showed payroll employment growth still positive, with the unemployment rate around 4.3%, indicating a labor market that continues to outperform earlier recession-oriented forecasts. Average hourly earnings growth and steady weekly hours suggest that underlying demand for labor remains solid, even as interest-sensitive sectors such as housing and some areas of business investment show signs of cooling.

Regional patterns are uneven. Advanced economies generally show slower growth as higher rates weigh on consumption and investment, while some emerging markets have benefited from trade flows, commodity trends and their positioning in global supply chains. Differences in fiscal capacity, energy exposure and policy choices are contributing to diverging outcomes across countries.

Inflation remains sticky, and central banks are cautious

Inflation readings around June kept the focus on “sticky inflation.” In the United States, the annual inflation rate rose to 4.2% in May 2026, up from 3.7% in April, marking the highest reading since April 2023 and the third consecutive monthly acceleration in headline inflation. Energy prices played a significant role, with gasoline and fuel oil posting sharp year-over-year gains following supply disruptions and elevated geopolitical tensions in the Middle East.

Core inflation, excluding food and energy, has been more contained but remains above the Federal Reserve’s 2% target. Core consumer prices were up 2.9% year over year in May, the highest level since late 2025, even as the month-to-month pace eased slightly compared with earlier in the spring. On a global basis, inflation indicators for advanced economies show ongoing effects from the energy shock, limited evidence of a broad wage-price spiral and some stabilization in survey-based measures of price expectations.

These dynamics leave central banks in a cautious stance. With inflation still above target and growth not yet signaling a clear downturn, policymakers are balancing the risk of cutting rates too soon and reigniting inflation against the drag that sustained higher rates can impose on economic activity. By the end of June, market expectations for the timing and scale of rate cuts had become more measured, reflecting both the recent uptick in inflation data and the continued resilience of labor markets.

Broadening equity rally: small caps and emerging markets lead

Equity markets in June reflected a continuation of themes that have defined the first half of 2026, but with meaningful rotation beneath the surface. Global equities delivered mixed results during the month, with European markets generally outperforming the United States and parts of Asia, and sector performance rotating away from the largest technology names toward more cyclical and value-oriented areas. Within the U.S., performance patterns indicate a shift away from previously dominant mega-cap growth stocks and toward smaller companies and nontechnology sectors.

Across the full first half of the year, the strength of small-cap stocks stands out. The Russell 2000 Index, a widely used benchmark for U.S. small caps, was up more than 22% for the year to date, putting it on pace for its best first half since 1991. In addition to the strong start to 2026, small caps are up about 41% over the prior 12-month period, underscoring the magnitude of the rebound after several years of underperformance relative to large caps. These gains highlight renewed investor interest in more domestically focused, economically sensitive companies as recession fears have eased and earnings expectations have improved.

Emerging market equities have also delivered strong results. In the first half of 2026, emerging market equities rose approximately 24%, outpacing developed markets and benefiting from gains in technology-heavy markets and export-oriented economies tied into global supply chains. Many of the biggest equity winners in the first half of 2026 were outside the United States, including non-U.S. technology and semiconductor names that participated in the same artificial intelligence and digital infrastructure themes driving U.S. markets.

Taken together, a roughly 22.7% gain in small caps and a 24% gain in emerging markets through June 30 signal a meaningful broadening of equity leadership beyond a narrow group of U.S. mega-cap technology stocks. This broadening has unfolded alongside modest but positive global growth, persistent yet evolving inflation dynamics and shifting expectations for future monetary policy. The first half of 2026 stands out as a period in which investors rewarded a wider range of regions, sectors and company sizes than in the recent past, even as markets remained sensitive to geopolitical developments and economic data.

Closing thoughts

June 2026 closed a first half defined by resilience, crosscurrents and rotation. The global economy has slowed but remains on a growth path, inflation continues to run above central bank targets and equity markets have delivered strong returns, particularly in small caps and emerging markets, as leadership broadened beyond a narrow set of large U.S. technology names.

We will continue to monitor economic data, inflation trends, policy decisions and market behavior in the months ahead and will keep you informed through future communications. Thank you for your continued trust and for the opportunity to serve as stewards of your capital.

This market commentary is meant for informational and educational purposes only and does not consider any individual personal considerations. As such, the information contained herein is not intended to be personal investment advice or a recommendation of any kind. The commentary represents an assessment of the market environment through May 2026.

The views and opinions expressed may change based on the market or other conditions. The forward-looking statements are based on certain assumptions, but there can be no assurance that forward-looking statements will materialize.

Equity securities are subject to price fluctuation and investments made in small and mid-cap companies generally involve a higher degree of risk and volatility than investments in large-cap companies. International securities are generally subject to increased risks, including currency fluctuations and social, economic, and political uncertainties, which could increase volatility. These risks are magnified in emerging markets.

Fixed-income securities are subject to loss of principal during periods of rising interest rates and are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications, and other factors before investing. Interest rates and bond prices tend to move in opposite directions. When interest rates fall, bond prices typically rise, and conversely, when interest rates rise, bond prices typically fall.

There is no assurance that any investment, plan, or strategy will be successful. Investing involves risk, including the possible loss of principal. Past performance does not guarantee future results, and nothing herein should be interpreted as an indication of future performance. Please consult your financial professional before making any investment or financial decisions.

AdvicePeriod is another business name and brand utilized by both Mariner, LLC and Mariner Platform Solutions, LLC, each of which is an SEC registered investment adviser. Registration of an investment adviser does not imply a certain level of skill or training. For additional information about Mariner, LLC or Mariner Platform Solutions, LLC, including fees and services, please contact us utilizing the contact information provided herein or refer to the Investment Adviser Public Disclosure website (www.adviserinfo.sec.gov).

For additional information as to which entity your adviser is registered as an investment adviser representative, please refer to the Investment Adviser Public Disclosure website (www.adviserinfo.sec.gov) or the Form ADV 2B provided to you. Investment adviser representatives of Mariner, LLC are generally employees. Investment adviser representatives of Mariner Platform Solutions, LLC dba AdvicePeriod, are independent contractors.

Indexes referenced are unmanaged and cannot be directly invested into. For index definitions visit https://www.marinerwealthadvisors.com/index-definitions/.

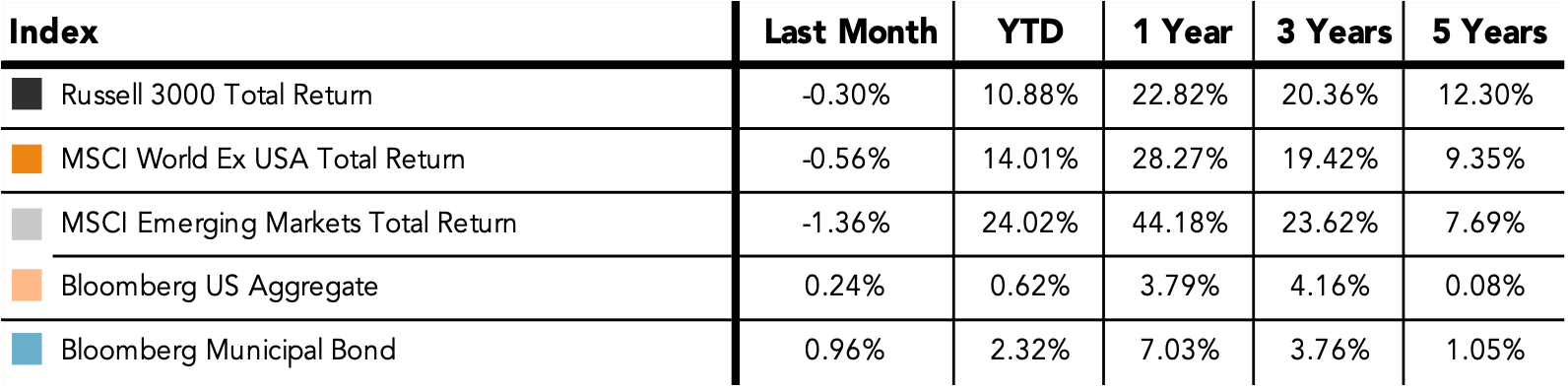

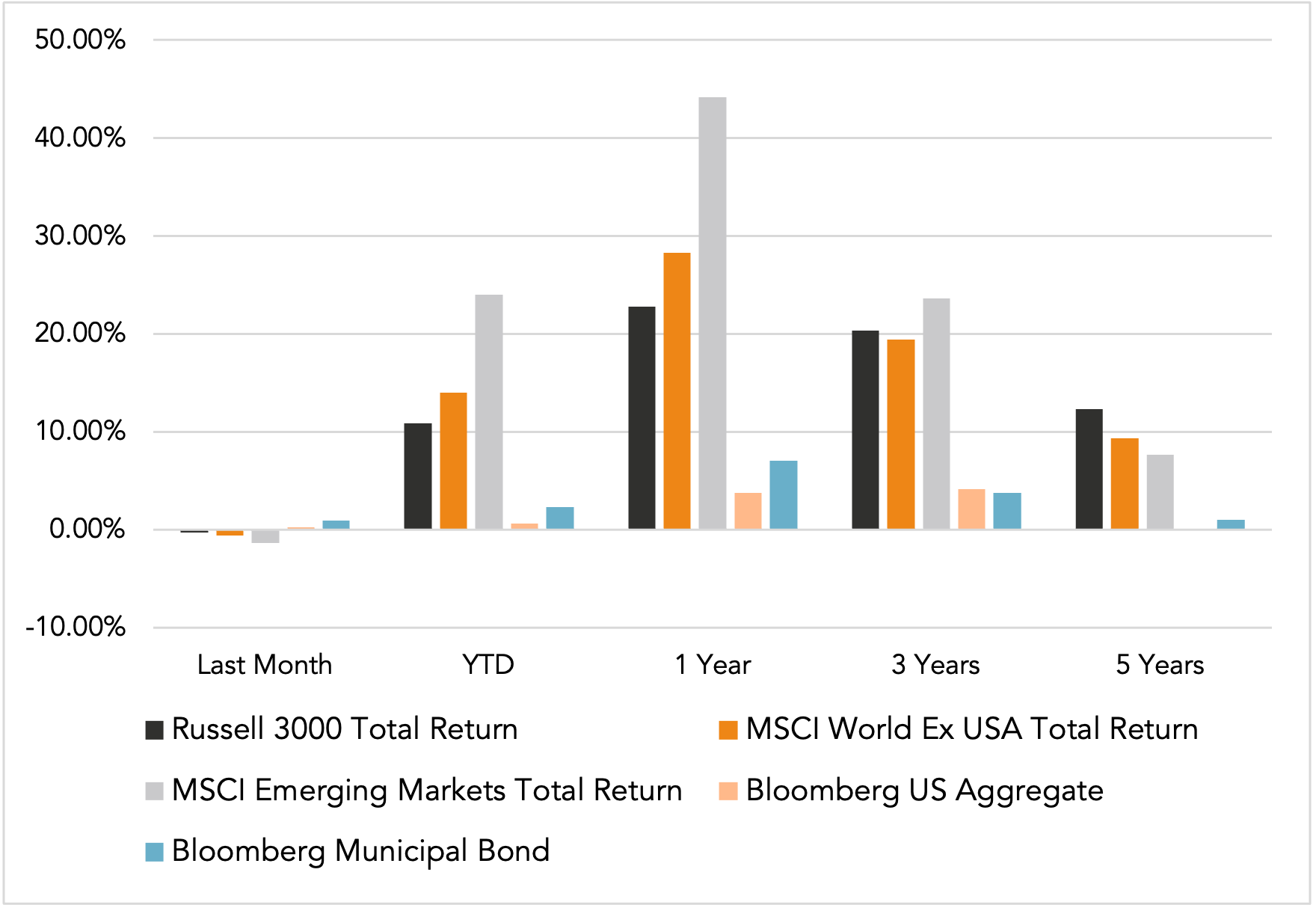

Does past performance matter?

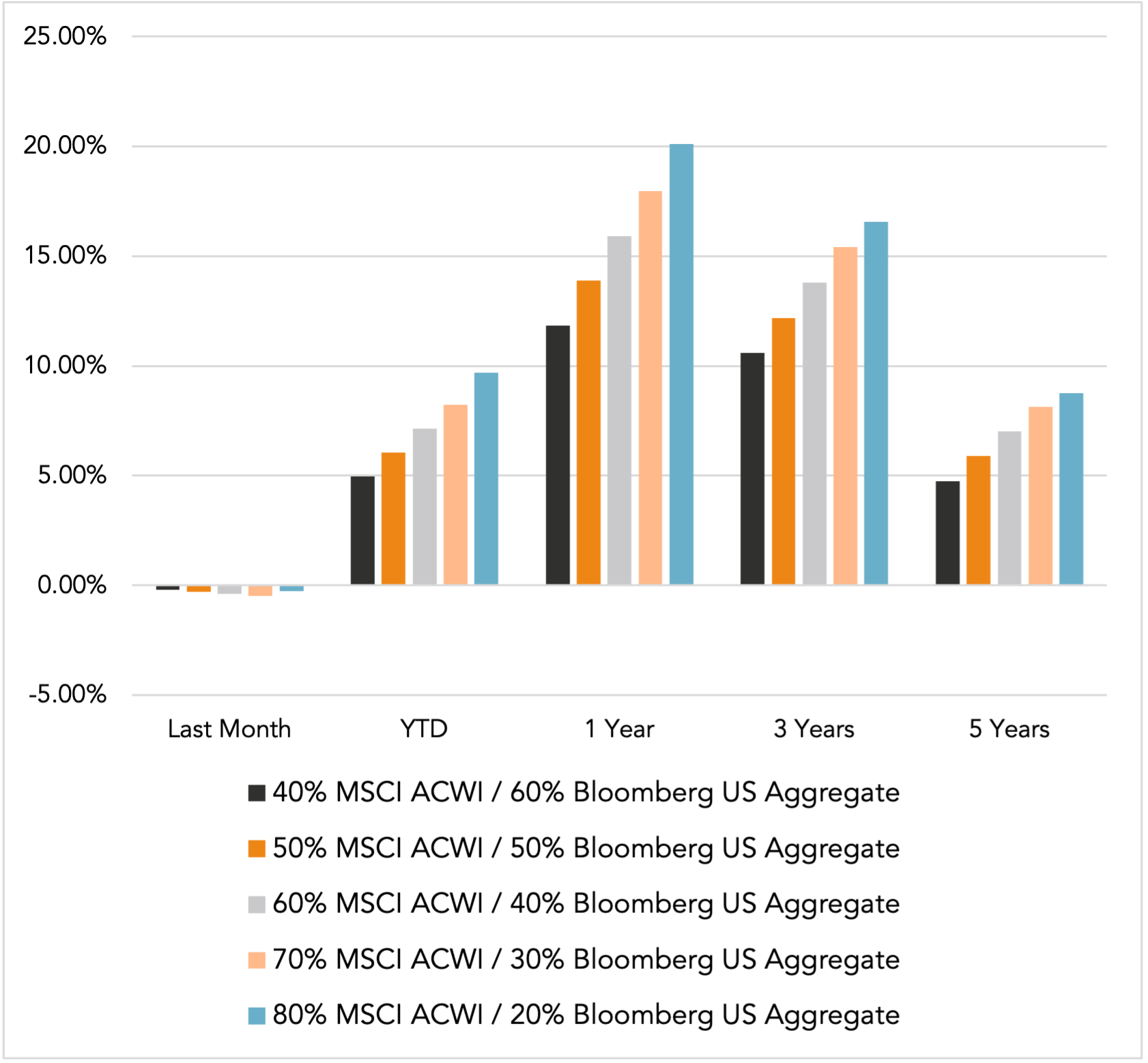

Major Market Index Returns

Period Ending 6/1/2026

Multi-year returns are annualized.

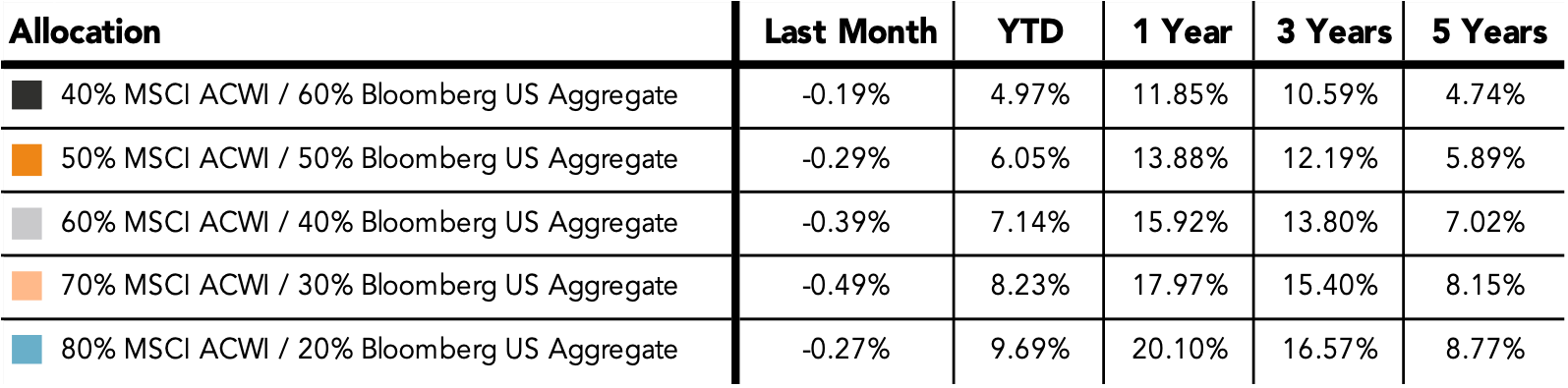

Mix Index Returns

Global Equity / US Taxable Bonds

Indexes are unmanaged and cannot be directly invested into. Past performance is no indication of future results. Investing involves risk and the potential to lose principal.

The Russell 3000 Index is a United States market index that tracks the 3000 largest companies. MSCI Emerging Markets Index is a broad market cap-weighted Index showing the performance of equities across 23 emerging market countries defined as emerging markets by MSCI. MSCI ACWI ex-U.S. Index is a free-float adjusted market capitalization-weighted index that is designed to measure the equity market performance of developed and emerging markets excluding companies based in the United States. Bloomberg U.S. Aggregate Bond Index represents the investment-grade, U.S. dollar-denominated, fixed-rate taxable bond market, including Treasuries, government-related and corporate securities, as well as mortgage and asset-backed securities. Bloomberg Municipal Index is the US Municipal Index that covers the US dollar-denominated long-term tax-exempt bond market. The index has four main sectors: state and local general obligation bonds, revenue bonds, insured bonds, and prerefunded bonds.

Monthly Market Update – May 2026