We have been asked how the current debt ceiling conundrum and associated congressional debates on this subject impact your outlook on the financial markets. We think this is a summer item that will be resolved in “less-than-perfect, yet adequate fashion.” While a temporary issue that will likely be adequately resolved, the volatility the debt ceiling can inspire is one of the reasons we maintain a neutral, “hold your ground” stance for the near term. This concern should be behind us by mid-summer.

Yes, the U.S. stock market sold off nearly 20% in the second half of 2011 when the U.S. debt was downgraded, and that saw the S&P 500 end the full calendar year essentially flat.5 For some reason, this period is what comes to investors’ minds when they hear the phrase “debt ceiling discussions,” much like the negative reflex reaction of immediately envisioning the ugly 1970’s bear market in stocks when one reads about elevated inflationary pressures. However, the 2011 calendar year pullback inspired by fiscal concerns came on the heels of strong stock market returns in 2009, 2010 and in the first half of 2011.6 This is the opposite of the case today, with these discussions arising in the aftermath of a horrible stock market in 2022, and a lot of negative news has been discounted in advance. The precursor performance stage couldn’t be more different going into these congressional discussions versus 2011.

In addition, 2011 was about much more than fiscal debates in the U.S. The world was approaching the apex in a global financial crisis centered on Europe back then. Remember the so-called “PIIGS” countries (Portugal, Italy, Ireland, Greece and Spain), which were working through massive deficits and debt restructurings that required bailouts from the European Union and International Monetary Fund? There were mass protests in these countries related to the austerity measures and tax increases needed to fix this crisis overseas—scary stuff! Spreads were surging on the debt of these foreign countries, and it was a mess on a global scale, which all compounded to impact investor mood that year. Despite all this, the U.S. stock market went on to achieve new highs by April 2012, just a few months after the U.S. debt downgrade, and successful measures were employed to avoid worst-case outcomes in Europe. Hopefully, this provides perspective on the far more benign environment today as these debates begin to play out in Washington.

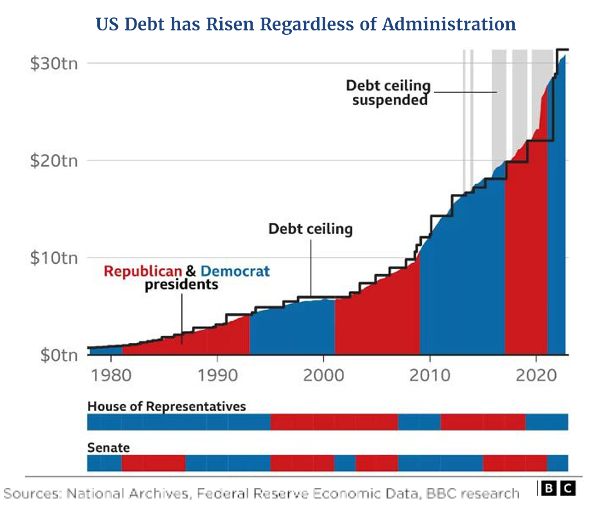

In truth, the concept of a debt ceiling is really a silly thing, as it is not coordinated with the annual government budget resolutions and spending approvals. The spending bills are passed in Congress with full knowledge by all that the approved spending targets will absolutely breach the debt ceiling limits in due time. In our opinion, both parties use the ceiling as a bargaining chip to get their legislation agenda items passed, i.e., “If you want X, you need me to vote to raise the debt ceiling, and I’ll do that if you give me Y.” Eventually someone blinks, agreement is reached and “crisis” is avoided. Both parties have raised or suspended the debt ceiling numerous times going back to the 1980s, and they have done so 20 times alone since 2002! This gamesmanship has become a tradition and clearly is tiresome to us all.

This year is no different. What are the general impacts of all this congressional theater? The data shows that historically, volatility in the stock market increases in the months leading up to the debt ceiling violation date (the X date). Shortly after the eventual vote to suspend it for a period or raise it, volatility stabilizes and resumes prior levels.

Options and Potential Outcomes

Scenario 1: Eventual Bipartisan Passage of a Plan to Lift the Debt Ceiling—Likely.

The GOP members of the House are passionate about lowering the deficit and cutting spending, and they have successfully passed such belt- tightening legislation as part of a debt ceiling package in the House chamber. With a thin majority in the House, it is pretty impressive that they were able to do this, and it actually increases the odds of a bill eventually getting through the Senate and approved by the White House, despite what you may read. No doubt this House bill will be watered down in the Senate. There will probably be some extended brinkmanship here as Senate Democrats and the Biden administration push for a clean debt ceiling increase with no or limited spending cuts. Fortunately, leaders on both sides of the aisle in the Senate support raising the debt ceiling in general, so watered-down bipartisan passage in the House and Senate is possible and likely to occur at the eleventh hour.

Scenario 2: House and Senate Suspend the Debt Ceiling Limit for a Time—Somewhat Likely

There could be some type of legislative action approved in the House and Senate in bipartisan fashion to temporarily suspend the debt ceiling and give the government some breathing room to figure things out with a pledge to do so by some committed date in the future. Like the scenario above, this would relieve the markets, though this too will incur drama and likely come at the eleventh hour. No doubt this simply kicks the can down the road, as is often the case.

Other less likely scenarios include the option for the president to raise the debt limit subject to a congressional motion of disapproval, which he then could veto. This strategy was used by Obama back in 2011 to negotiate with congressional leaders to extend the debt limit until 2013 in conjunction with a pledge to agree to budget cuts by a certain date or face automatic cuts known as “sequestration.” The market was comfortable with this resolution, just as it would be with the others above, but experts we talk to don’t believe this option is the likely path this time.

While contentious partisan politics does raise the remote risk of a credit rating agency downgrade of U.S. debt, à la the 2011 variety, we think this is unlikely as well. We find it noteworthy that credit rating agencies in 2011 were threatening downgrades for months in advance and now they seem significantly less concerned, suggesting that they now understand the political posturing is temporary. Should a downgrade occur, however, it would be a catalyst to quickly pass a resolution to lift or suspend the debt ceiling and ultimately resolve the issue. Market reaction and discipline would, in essence, force a resolution quickly if this happened. This is the least comfortable path from our perspective, although it would not derail our belief that stocks will advance later in 2023 and on into 2024.

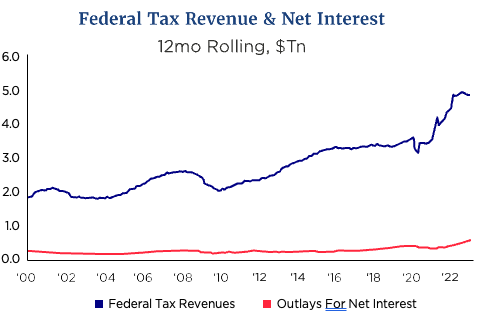

More extreme questions we get include our thoughts as to whether this drama risks a default on U.S. debt. We have never experienced a default on U.S. debt despite the more than 20 debt ceiling debates/raises since 2002 alone. The reason for this is compelling: U.S. government cash flow is adequate to comfortably cover the interest on U.S. debt.

Source: Strategas

Bottom line, we see this issue as a not-uncommon occurrence that has been resolved in a handful of different ways over the course of time. We think the same will happen this summer when the X date approaches in the June/July time frame. It will create some heightened volatility that supports our “hold your ground” view on stocks in the near term but should not have lasting negative economic or market impact.

Footnotes:

The S&P 500 Index is a market-value weighted index provided by Standard & Poor’s and is comprised of 500 companies chosen for market size and industry group representation. The index is unmanaged and cannot be directly invested into. Investing involves risk and the potential to lose principal. Past performance does not guarantee future results.

This commentary is limited to the dissemination of general information pertaining to general economic market conditions. The views expressed are for commentary purposes only and do not take into account any individual personal, financial, or tax considerations. As such, the information contained herein is not intended to be personal legal, investment, or tax advice or a solicitation to buy or sell any security or engage in a particular investment strategy. Nothing herein should be relied upon as such, and there is no guarantee that any claims made will come to pass. Any opinions and forecasts contained herein are based on the information and sources of information deemed to be reliable, but Mariner Advisor Network’s does not warrant the accuracy of the information that any opinion or forecast is based upon. You should note that the materials are provided “as is” without any express or implied warranties. Opinions expressed are subject to change without notice and are not intended as investment advice or to predict future performance. Consult your financial professional before making any investment decision.

Mariner Wealth Advisors is the parent company of Mariner Advisor Network, MIAN and MPS.

Jeff Krumpelman, CFA

Chief Investment Strategist and Head of Equities with Mariner Wealth Advisors.

Disclosures:

AdvicePeriod is another business name and brand utilized by both Mariner, LLC and Mariner Platform Solutions, LLC, each of which is an SEC registered investment adviser. Registration of an investment adviser does not imply a certain level of skill or training. Each firm is in compliance with the current notice filing requirements imposed upon SEC registered investment advisers by those states in which each firm maintains clients. Each firm may only transact business in those states in which it is notice filed or qualifies for an exemption or exclusion from notice filing requirements. Any subsequent, direct communication by an advisor with a prospective client shall be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides. For additional information about Mariner, LLC or Mariner Platform Solutions, LLC, including fees and services, please contact us utilizing the contact information provided herein or refer to the Investment Adviser Public Disclosure website (www.adviserinfo.sec.gov). Please read the disclosure statement carefully before you invest or send money.

For additional information as to which entity your adviser is registered as an investment adviser representative, please refer to the Investment Adviser Public Disclosure website (www.adviserinfo.sec.gov) or the Form ADV 2B provided to you. Investment adviser representatives of Mariner, LLC dba Mariner Wealth Advisors and dba AdvicePeriod are generally employed by Mariner Wealth Advisors, LLC. Investment adviser representatives of Mariner Platform Solutions, LLC dba AdvicePeriod, are independent contractors.