Please find our most recent market review below. We hope these perspectives are valuable to you.

– The AdvicePeriod Team

Key observations

- The war involving Iran has heightened geopolitical risk, causing volatility and a flight to safe‑haven assets. It has also pushed oil prices higher, lifting inflation expectations and fueling stagflation fears.

- Rising energy prices, partly linked to the conflict, added to existing price pressures and pushed inflation expectations higher. This re‑acceleration has kept uncertainty elevated about the future path of interest rates and economic growth.

- U.S. equities swung sharply throughout March as investors reacted to war headlines and inflation concerns. A powerful rally in the final sessions of the month helped major indexes recover much of their earlier losses.

U.S. markets in March 2026 were dominated by the war in Iran, a sharp rise in energy prices and inflation expectations, and a volatile but ultimately resilient U.S. equity market. These dynamics created a challenging backdrop but did not fundamentally derail the underlying U.S. economic expansion as of month‑end.

Iran war, energy shock and sentiment

The most consequential development for markets in March was the ongoing war centered on Iran and the closure or disruption of shipping through the Strait of Hormuz, a key chokepoint for global oil and liquefied natural gas (LNG) flows. The conflict curtailed roughly 20% of global oil supply moving through the strait, prompting what the International Energy Agency has described as one of the most severe energy supply disruptions on record.

Energy prices responded quickly. Brent crude oil, the global benchmark, climbed from about $72 to $73 dollars per barrel in late February to more than $110 by late March, a rise of roughly 50% to 55% over the period. In the United States, gasoline prices moved higher as well, with nationwide averages pushing noticeably above early‑year levels and, in many areas, back above $3 per gallon.

This energy shock weighed on risk appetite. Equity markets around the world experienced bouts of selling pressure, while traditional safe‑haven assets such as U.S. Treasuries and the dollar saw periods of strong demand. Investor sentiment oscillated between hope for a negotiated off‑ramp and concern that a prolonged conflict could echo prior energy‑driven slowdowns, contributing to elevated day‑to‑day volatility through the month.

Inflation pressures re‑accelerating

Even before the latest spike in oil prices, U.S. inflation had settled into a range slightly above the Federal Reserve’s 2% target. The Consumer Price Index (CPI) for the 12 months ending in February 2026 increased 2.4%, unchanged from January and the lowest annual rate since mid‑2025. Core CPI, which excludes food and energy, rose 2.5% over the same period, also steady compared with the prior month.

Beneath those headline figures, key components such as food and shelter remained firm: food prices were up about 3.1% year over year and shelter up roughly 3.0% as of February. Meanwhile, some goods categories, including used cars and trucks, continued to exert modest disinflationary pressure as prices fell compared with a year earlier.

The war‑driven jump in energy prices altered inflation expectations for March and beyond. Market‑based measures and survey‑based forecasts began to converge around CPI readings in the low 3% range for the 12 months through March, versus the 2.4% rate observed through February. Analysts increasingly expected that the combination of higher oil and gas prices and still‑firm services inflation could keep headline inflation above 3% in the near term, even if core inflation trends eased only gradually.

This backdrop complicated the policy outlook. While the February data alone would have supported a narrative of gently cooling inflation, the March energy shock reintroduced concern that inflation could re‑accelerate or remain sticky at levels above the Federal Reserve’s target for longer than previously expected. As a result, investors trimmed expectations for near‑term interest‑rate cuts and, in some scenarios, began to consider the possibility that rates might need to remain restrictive for an extended period.

Choppy U.S. stocks with a late‑month surge

U.S. equity markets spent most of March under pressure, with most major indices recording notable swings as investors digested war headlines and higher oil prices. By late in the month, however, signs of tentative progress on the diplomatic front and some easing in the most extreme energy‑price fears helped stocks rebound, leaving the overall monthly decline milder than mid‑month levels had implied.

The overall pattern for March was one of elevated intramonth volatility followed by stabilization and a late‑month rally. Sector performance was uneven: energy and select commodity‑linked and defense‑related names outperformed on the back of higher input prices and geopolitical demand, while rate‑sensitive areas and some high‑growth technology stocks lagged.

Despite the shocks, the U.S. economic data backdrop remained relatively stable through the latest published releases. Real‑time indicators still pointed to moderate growth, supported by resilient consumer spending and labor‑market conditions, even as higher gasoline and food prices threatened to squeeze household budgets over time. For now, markets are balancing the near‑term drag from the energy shock and geopolitical uncertainty against the underlying strength of the domestic economy and expectations that policymakers will adjust as needed if conditions materially deteriorate.

We are closely following developments in the Middle East, the trajectory of inflation and how markets are digesting these events, with an eye on what truly matters over full cycles rather than individual headlines. Our team remains grounded in a disciplined, long‑term investment process so that portfolios stay aligned with your objectives even as conditions evolve.

This market commentary is meant for informational and educational purposes only and does not consider any individual personal considerations. As such, the information contained herein is not intended to be personal investment advice or a recommendation of any kind. The commentary represents an assessment of the market environment through December 2025.

The views and opinions expressed may change based on the market or other conditions. The forward-looking statements are based on certain assumptions, but there can be no assurance that forward-looking statements will materialize.

Equity securities are subject to price fluctuation and investments made in small and mid-cap companies generally involve a higher degree of risk and volatility than investments in large-cap companies. International securities are generally subject to increased risks, including currency fluctuations and social, economic, and political uncertainties, which could increase volatility. These risks are magnified in emerging markets.

Fixed-income securities are subject to loss of principal during periods of rising interest rates and are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications, and other factors. Interest rates and bond prices tend to move in opposite directions. When interest rates fall, bond prices typically rise, and conversely, when interest rates rise, bond prices typically fall.

There is no assurance that any investment, plan, or strategy will be successful. Investing involves risk, including the possible loss of principal. Past performance does not guarantee future results, and nothing herein should be interpreted as an indication of future performance. Please consult your financial professional before making any investment or financial decisions.

AdvicePeriod is another business name and brand utilized by both Mariner, LLC and Mariner Platform Solutions, LLC, each of which is an SEC registered investment adviser. Registration of an investment adviser does not imply a certain level of skill or training. For additional information about Mariner, LLC or Mariner Platform Solutions, LLC, including fees and services, please contact us utilizing the contact information provided herein or refer to the Investment Adviser Public Disclosure website (www.adviserinfo.sec.gov).

For additional information as to which entity your adviser is registered as an investment adviser representative, please refer to the Investment Adviser Public Disclosure website (www.adviserinfo.sec.gov) or the Form ADV 2B provided to you. Investment adviser representatives of Mariner, LLC are generally employees. Investment adviser representatives of Mariner Platform Solutions, LLC dba AdvicePeriod, are independent contractors.

Indexes referenced are unmanaged and cannot be directly invested into. For index definitions visit https://www.marinerwealthadvisors.com/index-definitions/.

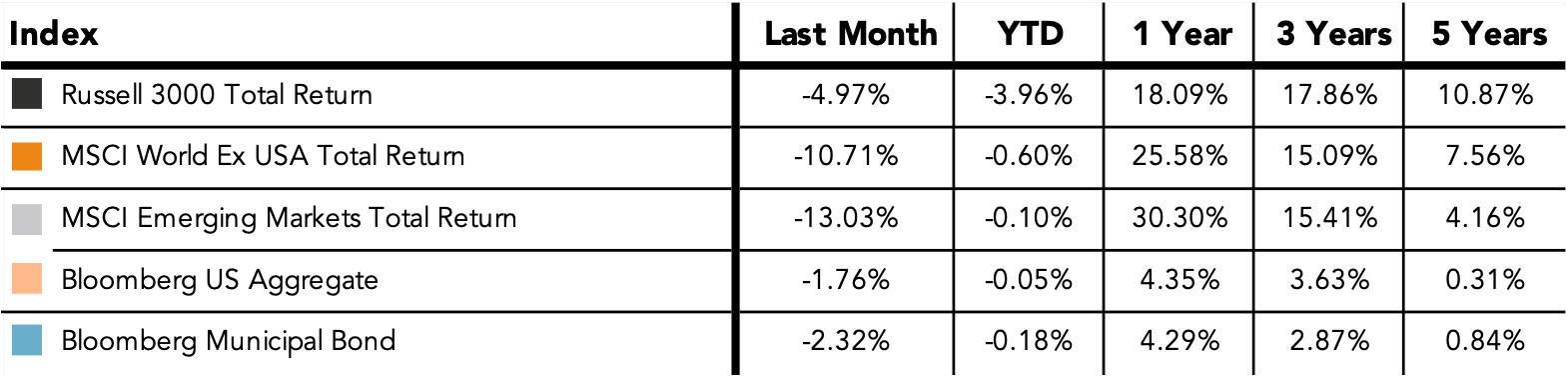

Does past performance matter?

Major Market Index Returns

Period Ending 3/1/2026

Multi-year returns are annualized.

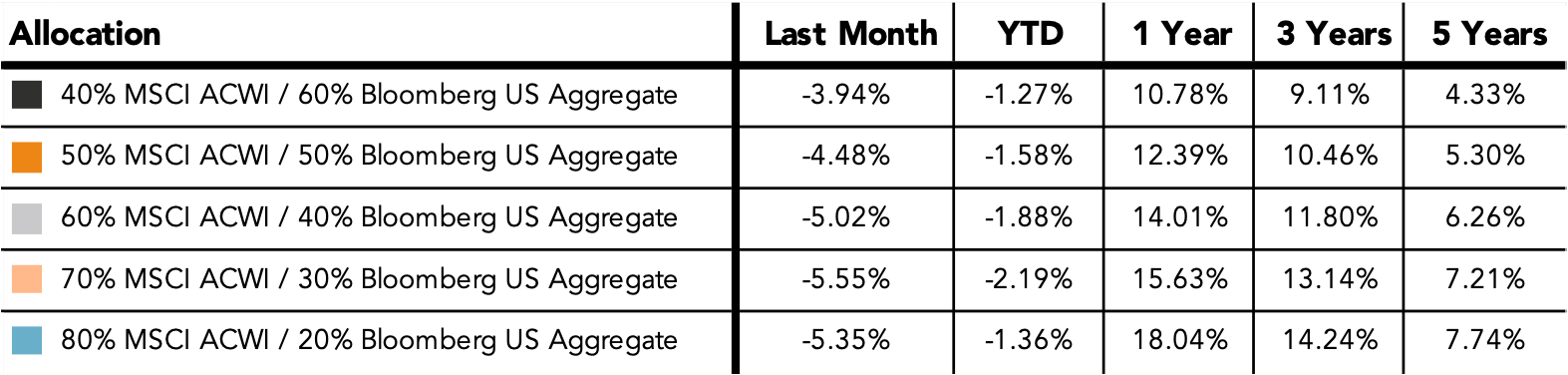

Mix Index Returns

Global Equity / US Taxable Bonds

Indexes are unmanaged and cannot be directly invested into. Past performance is no indication of future results. Investing involves risk and the potential to lose principal.

The Russell 3000 Index is a United States market index that tracks the 3000 largest companies. MSCI Emerging Markets Index is a broad market cap-weighted Index showing the performance of equities across 23 emerging market countries defined as emerging markets by MSCI. MSCI ACWI ex-U.S. Index is a free-float adjusted market capitalization-weighted index that is designed to measure the equity market performance of developed and emerging markets excluding companies based in the United States. Bloomberg U.S. Aggregate Bond Index represents the investment-grade, U.S. dollar-denominated, fixed-rate taxable bond market, including Treasuries, government-related and corporate securities, as well as mortgage and asset-backed securities. Bloomberg Municipal Index is the US Municipal Index that covers the US dollar-denominated long-term tax-exempt bond market. The index has four main sectors: state and local general obligation bonds, revenue bonds, insured bonds, and prerefunded bonds.

Monthly Market Update – February 2026