Please find our most recent market review below. We hope these perspectives are valuable to you.

– The AdvicePeriod Team

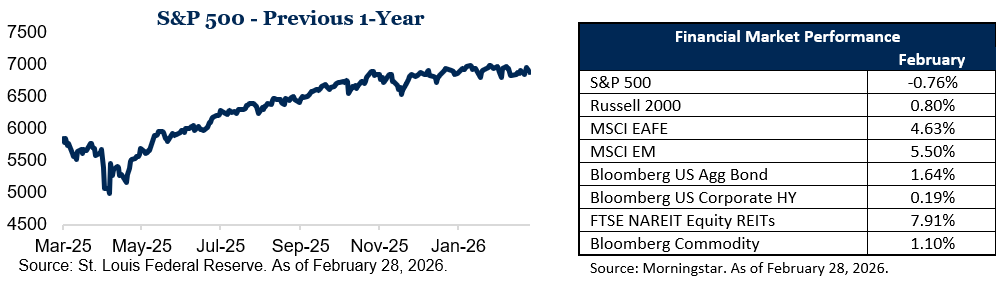

- February saw market gains spread beyond mega-cap tech, with mid-cap U.S., small-cap U.S., developed international, and emerging markets stocks all positive while the S&P 500 was down for the month. Domestically, value and cyclical areas such as energy, materials, and industrials led, showing growing confidence in the broader economy beyond artificial intelligence (AI).

- U.S.–Israeli airstrikes on Iran at the end of February injected a fresh layer of geopolitical risk into markets and raised concerns about a wider regional conflict. Fears of disruption in the Strait of Hormuz and a roughly 10% jump in crude prices pushed investors toward safe havens like gold and the U.S. dollar, clouding the near-term outlook.

- U.S. GDP data showed a slower pace of growth in Q4 2025, with softer consumer spending and a sharp drop in federal outlays after the government shutdown. At the same time, court challenges to President Trump’s tariffs and efforts to quickly reimpose them kept businesses cautious, even as consumer confidence ticked up from prior lows.

February 2026 was a month marked by improving market breadth, rising geopolitical tensions and softer—but still positive—economic data in the United States. In this update, we review how stocks and key sectors performed, how the emerging conflict involving Iran has affected market sentiment, and what recent economic reports suggest about the health of growth and inflation.

Equity Markets: Broader Participation Beyond Mega‑Cap Tech

After a year in which a small group of mega‑cap technology and AI–linked companies carried much of the market’s gains, February showed signs of healthier participation across a wider range of sectors and market capitalizations. Leadership broadened beyond the largest growth names, with equal weight, mid cap, and value exposures generally faring better than the narrow cohort of AI‑driven leaders that dominated earlier in the cycle.

Sector results underscored that theme. A majority of S&P 500 sectors finished the month in positive territory, with leadership coming from areas more directly tied to the real economy. Energy was a standout, posting strong gains as oil prices rose on the back of stronger demand expectations and growing geopolitical risk. Materials, consumer staples and industrials also posted solid advances, with returns in the mid‑ to high‑single‑digit range. These moves indicate that investors are increasingly willing to reward companies tied to manufacturing, commodities and everyday consumption, not just high‑growth technology names.

Breadth improved down the market‑cap spectrum as well. Commentary on U.S. small‑cap equities during February noted that, since late 2025, smaller companies have enjoyed periods of outperformance versus large caps as investors reassessed the outlook for interest rates and the domestic economy. While it is too early to say definitively whether this marks a lasting turning point for smaller stocks, the pattern in February was consistent with a market that is less narrowly dependent on a handful of mega‑cap leaders and more reflective of a broadening economic expansion.

Geopolitical Risk: Iran Conflict Adds a New Layer of Uncertainty

This broadening occurred against a backdrop of rapidly rising geopolitical tension late in the month. By the end of February, U.S. and Israeli strikes against Iran significantly escalated the long‑running standoff, raising concerns about the stability of the broader Middle East. Reports indicated that Iran threatened to close, and at times moved to effectively close, the Strait of Hormuz—a critical chokepoint through which roughly one‑fifth of the global oil supply transits each day.

The immediate market impact appeared most clearly in energy prices. Crude oil moved sharply higher as traders priced in the possibility of sustained disruption to regional production and shipping lanes. Some measures of crude showed prices surging more than 10% in a matter of days as tanker traffic slowed and shipping companies paused or rerouted voyages in response to the escalating conflict and increased risks in the Gulf.

For financial markets more broadly, the conflict has so far introduced an additional source of uncertainty rather than a clear directional signal. Higher oil and natural gas prices, if sustained, can raise input costs for businesses and reduce real purchasing power for consumers, potentially weighing on growth. At the same time, the overall equity response has been more measured than might be expected given the scale of geopolitical headlines, reflecting a view among some investors that disruptions could be temporary or mitigated by alternative supply and policy responses.

Safe‑haven behavior has been evident in currency and commodity markets. The U.S. dollar has benefited from safe‑haven demand, and gold has seen renewed interest as investors looked to hedge against tail‑risk scenarios. Together with existing questions around trade policy and tariffs, the Iran conflict has added another layer of complexity to the outlook, and the ultimate economic impact will depend heavily on whether energy‑market disruption proves brief or prolonged.

Economic Data: Slower Growth Amid Policy and Price Cross‑Currents

On the macroeconomic front, recent data show an environment of moderating yet positive growth in the U.S. The advance estimate for fourth‑quarter 2025 real GDP indicated that output grew at a slower pace than in the prior quarter and came in below consensus expectations. The deceleration was driven in large part by a sharp pullback in federal government spending, following a prolonged government shutdown, and by somewhat softer consumer demand compared with the earlier part of 2025.

Government spending acted as a significant swing factor in the numbers. Federal outlays dropped markedly in the quarter, and that decline alone subtracted approximately one percentage point from annualized GDP growth. Both defense and non‑defense spending retreated as agencies adjusted to the shutdown’s aftermath and operated under tighter budget constraints. Excluding the impact of this federal retrenchment, private‑sector activity appeared more resilient, with business investment—particularly in technology, automation and productivity‑enhancing projects—continuing to provide support.

Consumer spending remained the primary engine of growth but expanded at a slower pace than in the earlier post‑pandemic period. Households have been adjusting to cumulative price increases over the last several years and higher borrowing costs, even as wage growth and employment remain supportive. Some measures of inflation in late 2025 and early 2026 suggested that price pressures had cooled from their peaks but remained elevated in certain categories, leaving monetary policymakers balancing the goals of sustaining economic expansion while keeping inflation on a path toward their targets.

Developments in trade and tariff policy added another layer of cross‑currents. In February, the U.S. Supreme Court ruled that many of the tariffs imposed by President Trump in 2025 exceeded statutory authority, effectively blocking a significant portion of those levies. While in principle this ruling could reduce some cost pressures over time, the practical near‑term impact has been less straightforward. Some tariffs remain in place under other legal rationales, and there are active discussions within the administration about how to reshape trade measures within the bounds of the Court’s decision. As a result, businesses and consumers still face a shifting tariff environment, and economists expect elevated prices on certain imported goods to persist even as some tariffs are rescinded or restructured.

Survey data on households and businesses reflect this mixed picture. Households report feeling the strain of still‑elevated prices for essentials, even as they benefit from a labor market that has cooled gradually rather than abruptly. Business leaders, particularly in manufacturing and internationally exposed industries, cite uncertainty over trade rules and input costs as reasons for cautious planning, even as demand and order books remain generally healthy.

Putting the Month in Context

Taken together, February 2026 offered a more nuanced portrait of markets and the economy than simple “risk‑on” or “risk‑off” labels suggest. Equity performance showed encouraging breadth, with gains extending beyond a handful of mega‑cap technology names into a wider set of sectors and smaller companies. At the same time, the rapid escalation of the Iran conflict and the resulting jump in oil prices reminded investors how quickly geopolitics can reshape the risk landscape, particularly when key global supply routes are involved.

At the macroeconomic level, growth slowed but remained positive, with much of the weakness traceable to a one‑time adjustment in federal government spending after the shutdown rather than a broad deterioration in private‑sector fundamentals. Trade and tariff rulings, along with evolving policy responses, have kept the outlook for costs and margins in flux. This mix of broader market participation, elevated geopolitical and policy uncertainty and moderate growth defines the backdrop as we move further into 2026.

We will continue to monitor market breadth, geopolitical developments, and economic data as they evolve and to incorporate them into our view of the investment environment.

This market commentary is meant for informational and educational purposes only and does not consider any individual personal considerations. As such, the information contained herein is not intended to be personal investment advice or a recommendation of any kind. The commentary represents an assessment of the market environment through December 2025.

The views and opinions expressed may change based on the market or other conditions. The forward-looking statements are based on certain assumptions, but there can be no assurance that forward-looking statements will materialize.

Equity securities are subject to price fluctuation and investments made in small and mid-cap companies generally involve a higher degree of risk and volatility than investments in large-cap companies. International securities are generally subject to increased risks, including currency fluctuations and social, economic, and political uncertainties, which could increase volatility. These risks are magnified in emerging markets.

Fixed-income securities are subject to loss of principal during periods of rising interest rates and are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications, and other factors. Interest rates and bond prices tend to move in opposite directions. When interest rates fall, bond prices typically rise, and conversely, when interest rates rise, bond prices typically fall.

There is no assurance that any investment, plan, or strategy will be successful. Investing involves risk, including the possible loss of principal. Past performance does not guarantee future results, and nothing herein should be interpreted as an indication of future performance. Please consult your financial professional before making any investment or financial decisions.

AdvicePeriod is another business name and brand utilized by both Mariner, LLC and Mariner Platform Solutions, LLC, each of which is an SEC registered investment adviser. Registration of an investment adviser does not imply a certain level of skill or training. For additional information about Mariner, LLC or Mariner Platform Solutions, LLC, including fees and services, please contact us utilizing the contact information provided herein or refer to the Investment Adviser Public Disclosure website (www.adviserinfo.sec.gov).

For additional information as to which entity your adviser is registered as an investment adviser representative, please refer to the Investment Adviser Public Disclosure website (www.adviserinfo.sec.gov) or the Form ADV 2B provided to you. Investment adviser representatives of Mariner, LLC are generally employees. Investment adviser representatives of Mariner Platform Solutions, LLC dba AdvicePeriod, are independent contractors.

Indexes referenced are unmanaged and cannot be directly invested into. For index definitions visit https://www.marinerwealthadvisors.com/index-definitions/.

Does past performance matter?

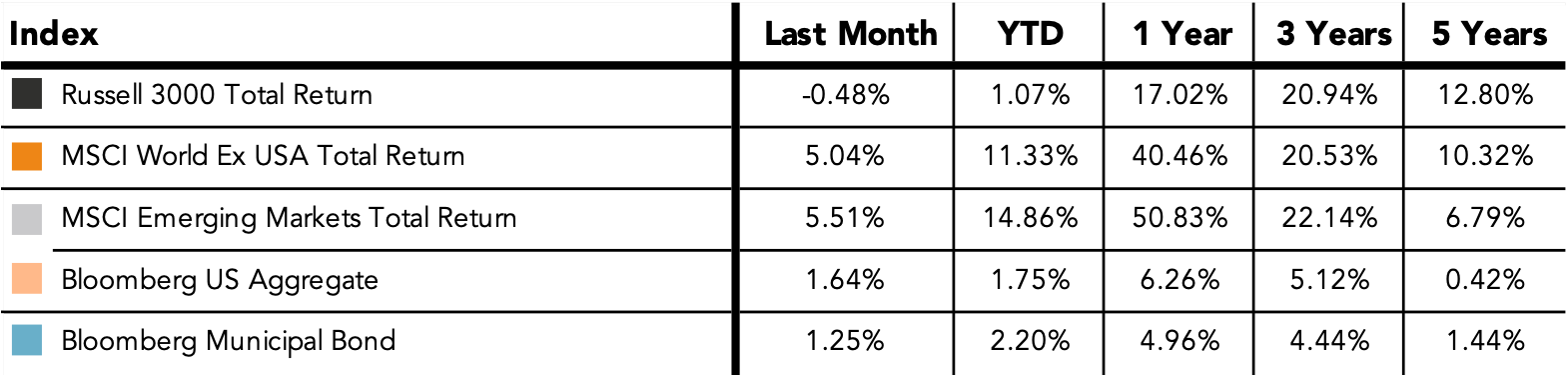

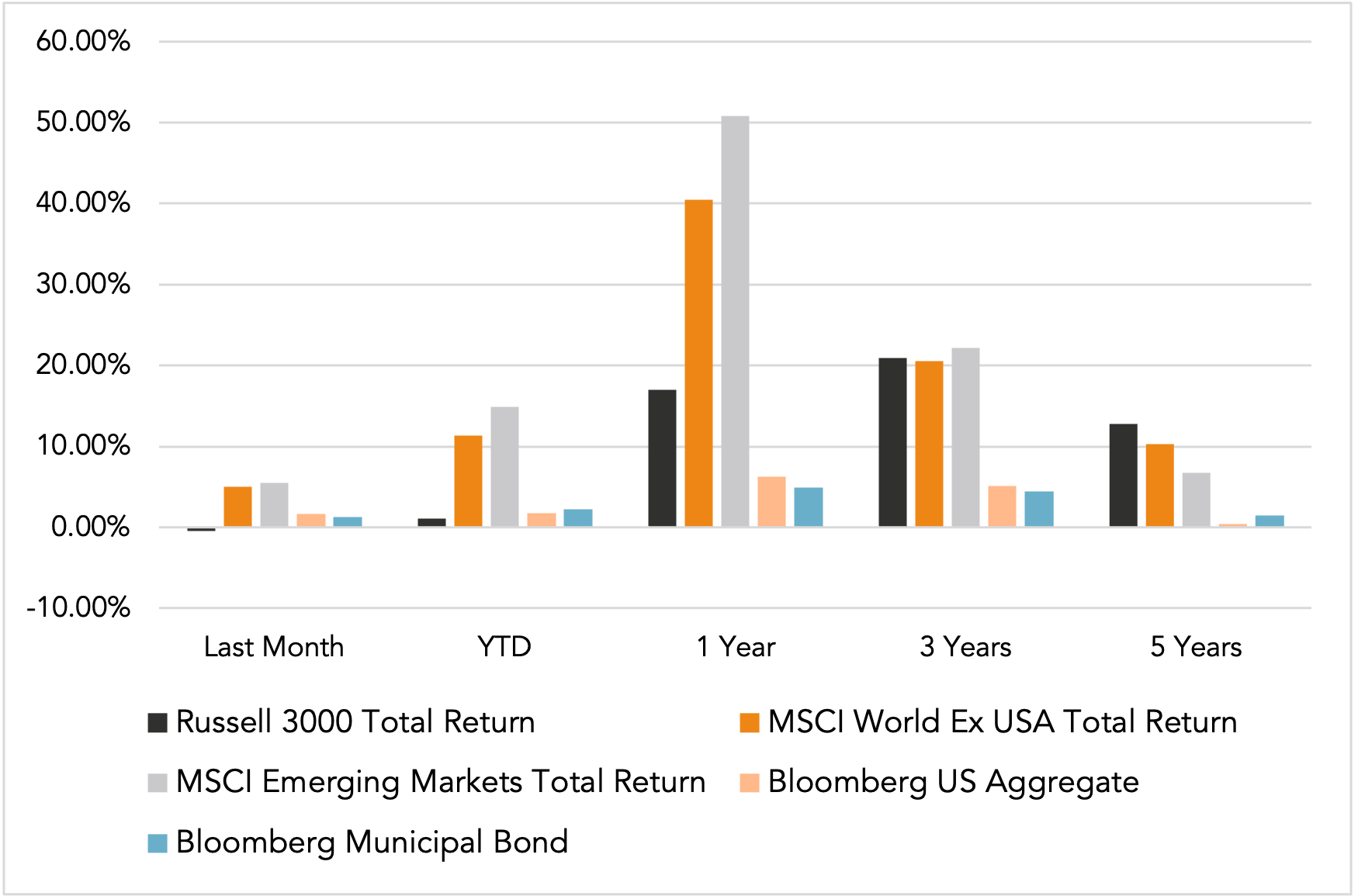

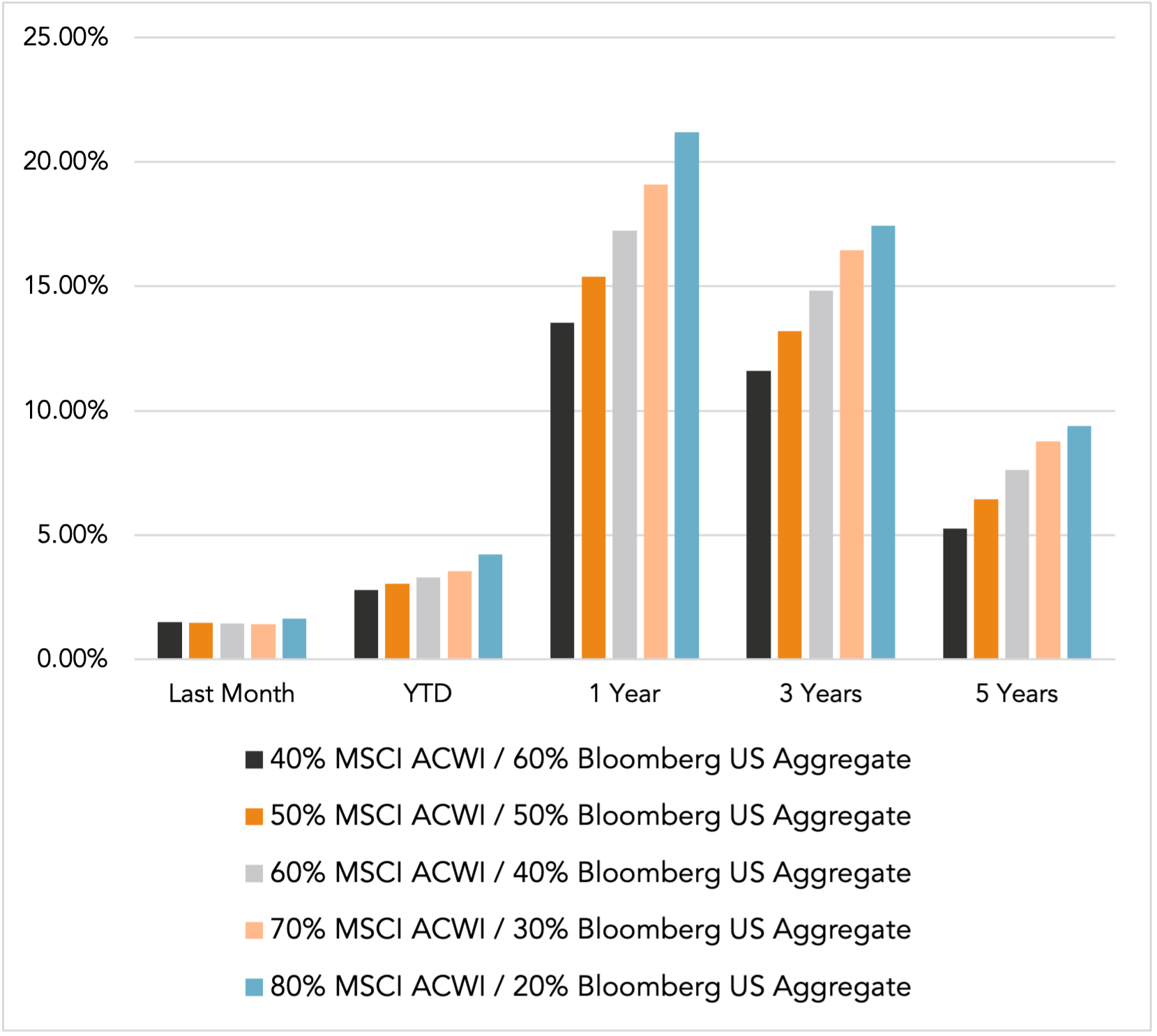

Major Market Index Returns

Period Ending 2/1/2026

Multi-year returns are annualized.

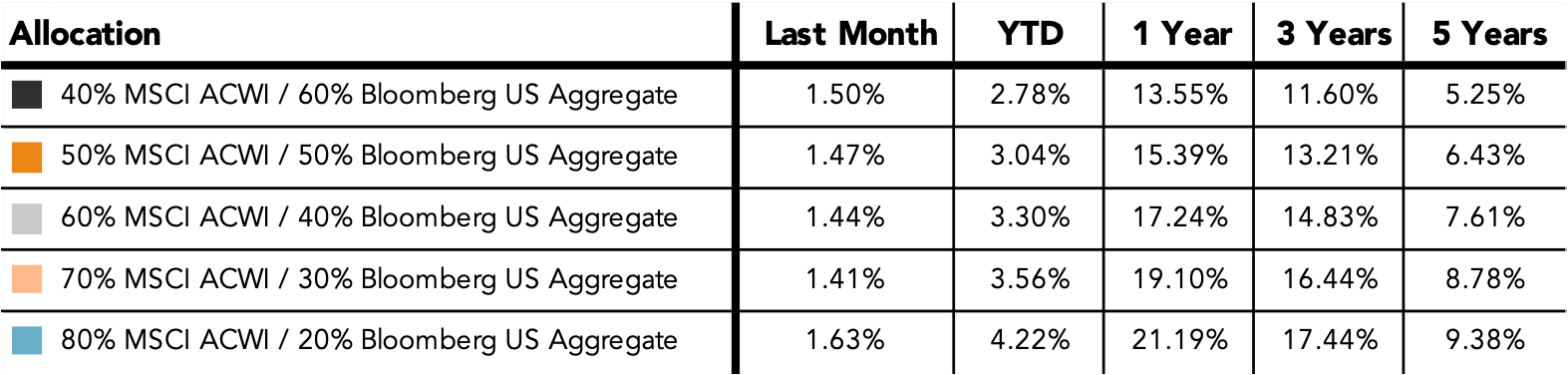

Mix Index Returns

Global Equity / US Taxable Bonds

Indexes are unmanaged and cannot be directly invested into. Past performance is no indication of future results. Investing involves risk and the potential to lose principal.

The Russell 3000 Index is a United States market index that tracks the 3000 largest companies. MSCI Emerging Markets Index is a broad market cap-weighted Index showing the performance of equities across 23 emerging market countries defined as emerging markets by MSCI. MSCI ACWI ex-U.S. Index is a free-float adjusted market capitalization-weighted index that is designed to measure the equity market performance of developed and emerging markets excluding companies based in the United States. Bloomberg U.S. Aggregate Bond Index represents the investment-grade, U.S. dollar-denominated, fixed-rate taxable bond market, including Treasuries, government-related and corporate securities, as well as mortgage and asset-backed securities. Bloomberg Municipal Index is the US Municipal Index that covers the US dollar-denominated long-term tax-exempt bond market. The index has four main sectors: state and local general obligation bonds, revenue bonds, insured bonds, and prerefunded bonds.

Monthly Market Update – April 2026