Please find our most recent market review below. We hope these perspectives are valuable to you.

– The AdvicePeriod Team

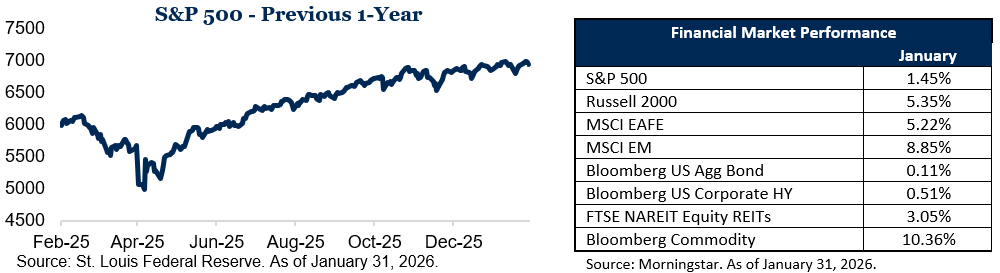

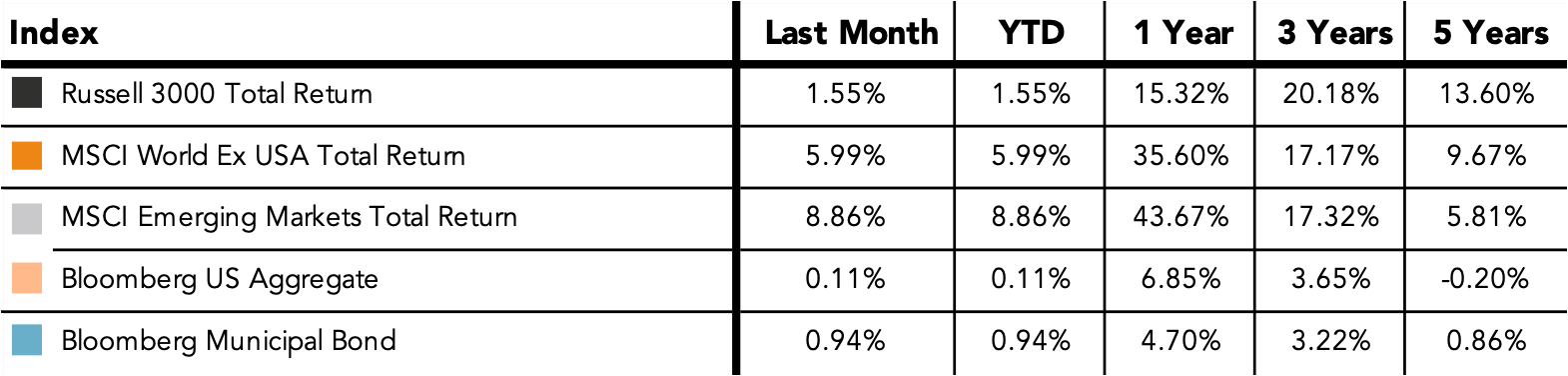

- U.S. stocks in January 2026 posted a modest gain, with the S&P 500 up 1.45% and setting or approaching new record highs, signaling continued optimism despite volatility.

- Inflation is hovering in the high‑2% range on Consumer Price Index (CPI) measures (around 2.7% year over year recently), with core CPI near 2.6%. Many analysts warn that underlying pressures could push inflation higher again later in 2026.

- The labor market has cooled significantly but remains tight: Recent data show monthly job gains around 50,000 with unemployment near 4.4%, indicating slower hiring but no sharp deterioration in employment conditions.

U.S. and global markets started 2026 on a generally positive but more cautious note. January brought modest equity gains, steady but not yet “finished” inflation and a labor market that continues to cool without showing signs of major stress.

Equity markets: A modestly positive start

The S&P 500 delivered a gain of roughly 1.45% in January 2026, extending the market’s three‑year winning streak and briefly approaching the 7,000 level during the month. While this advance is less dramatic than some recent rallies, it reflects an environment where investors are still willing to pay up for large‑cap U.S. equities despite higher interest rates and slower economic growth.

The index’s move was broad enough to keep the long‑running uptrend intact, even as day‑to‑day trading remained choppy around Federal Reserve communications and large technology earnings reports. Valuation measures such as the forward 12‑month price‑to‑earnings ratio for the S&P 500 remain above their five‑year averages, suggesting investors are still discounting solid earnings growth in 2026.

Under the surface, sector performance continued to reflect a “quality growth” bias. Companies with durable earnings, strong balance sheets and exposure to secular themes (such as technology and health care) generally fared better than more cyclical or highly leveraged businesses. At the same time, the modest overall index gain shows that investors are increasingly discriminating, rewarding firms that meet or beat earnings expectations and punishing those that disappoint.

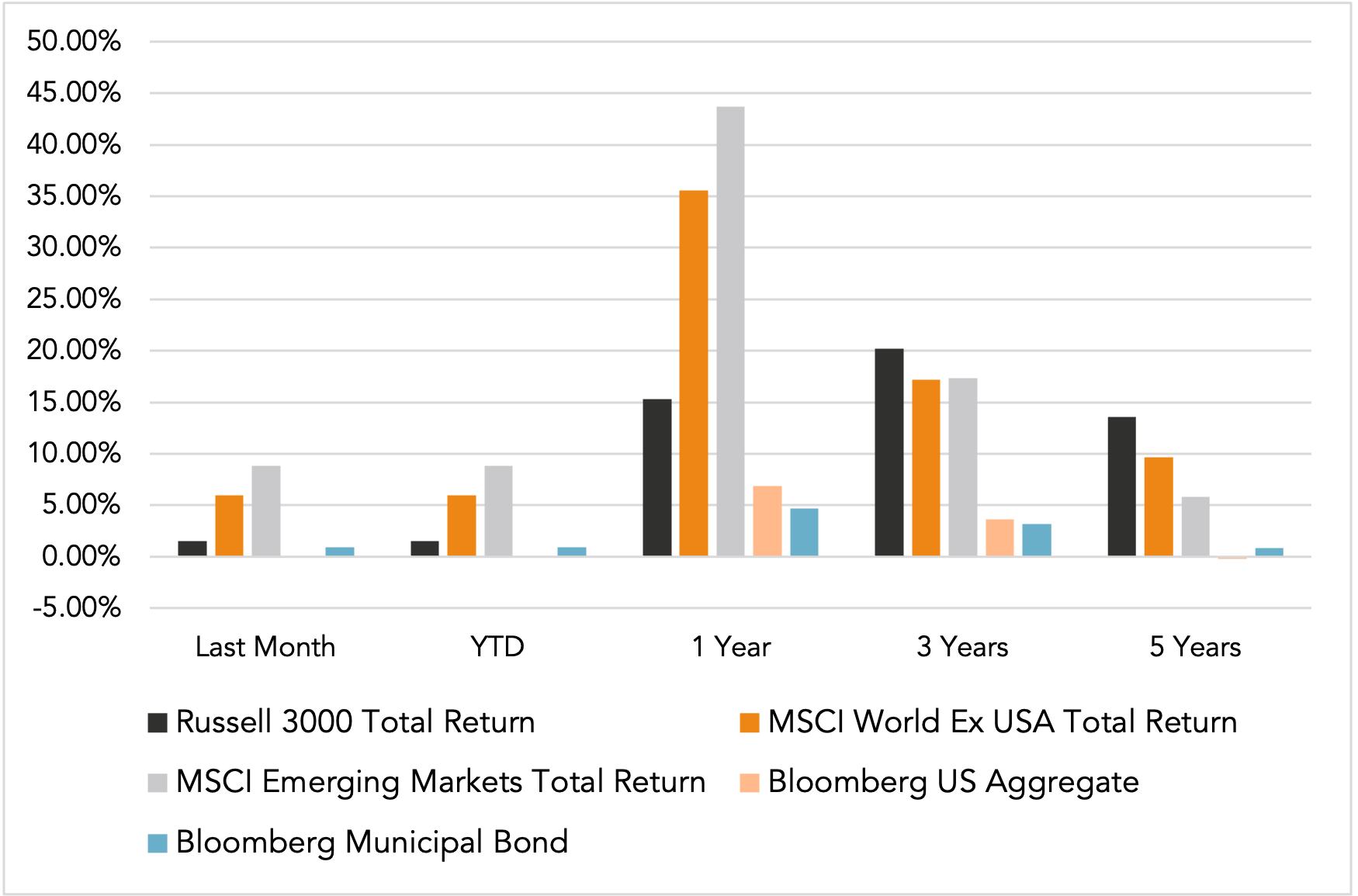

Internationally, performance was again ahead of returns here at home. For globally diversified investors, January’s pattern reinforced a dynamic that has been in place for over a year now. Coming off a much lower valuation, international equities have outpaced domestic, despite the dominance of the US tech sector in the headlines.

Inflation: Steady but not fully tamed

Inflation data available in January continued to show price pressures that are well below their 2022 peaks but still modestly above the Federal Reserve’s 2% target. The final Consumer Price Index (CPI) report for December 2025, released in mid‑January, confirmed that headline inflation finished 2025 at 2.7% year over year, with core inflation at about 2.6%.

Month to month, prices rose 0.3% in December, led by shelter and food, with energy also contributing to the increase. These details underscore an important nuance: While goods‑related inflation has largely cooled, key services categories—especially housing‑related costs—remain sticky and are likely to keep overall inflation from dropping sharply in the near term.

Policy and economic research groups highlighted that the 2025 inflation outcome was slightly better than some had feared but still high enough to keep real (inflation‑adjusted) interest rates positive. The risk of somewhat higher inflation later in 2026 remains, particularly if wage growth or housing costs re‑accelerate.

For investors, the key implication is that the “disinflation” process has progressed, but the environment is not yet back to the very low and stable inflation regime that prevailed for much of the 2010s. That reality matters for both bond and stock markets: Bond yields remain influenced by expectations for how quickly inflation converges to 2%, while equity valuations depend on the balance between earnings growth and the discount rate investors apply to those earnings. The nomination of Kevin Warsh as the new chair of the Federal Reserve could influence those expectations over the coming months as his confirmation approaches.

Labor market: Cooler, but still resilient

Labor market data released in January painted a picture of slower—but still positive—job growth as 2025 ended. The U.S. economy added about 50,000 nonfarm payroll jobs in December, a clear step down from the average monthly gains seen in 2024. At the same time, the unemployment rate edged down to 4.4%, indicating that while hiring has cooled, there has not been a sharp deterioration in overall employment conditions.

The December report showed job gains concentrated in areas such as health care, social assistance and food services, while sectors like retail trade shed jobs. Revisions to prior months lowered the estimated number of jobs created in October and November, reinforcing the message that the pace of labor market expansion has slowed meaningfully from earlier in the cycle.

Over the full year 2025, payroll increases averaged just under 50,000 per month, compared with roughly 168,000 per month in 2024, according to Bureau of Labor Statistics figures and related summaries. This deceleration is consistent with an economy working through the lagged effects of tighter monetary policy, as higher borrowing costs gradually feed through to corporate hiring and investment decisions.

A labor market growing at this slower pace can still support consumer spending, particularly if real wage growth (wages after inflation) remains positive. However, the margin for error has narrowed: A further slowdown from here could raise concerns about recession, while a re‑acceleration in wages without corresponding productivity gains could complicate the inflation outlook.

Putting the pieces together

Taken together, January’s information suggests an economy in a “late‑cycle” phase: growth is moderating, job creation has downshifted and inflation is closer to target but not fully anchored. In this setting, it’s notable that the equity market was still able to generate a positive return and maintain elevated valuation levels through the first month of the year.

For diversified investors, January 2026 did not bring a clear inflection point but rather a continuation of trends that have been building over the past year:

- U.S. equities remain supported by earnings and by the absence of a sharp economic downturn, even as volatility around policy and data persists.

- International equities continue to reward diversified investors.

- Inflation is lower and more predictable than it was earlier in the cycle, but key categories like shelter and services keep it modestly above target.

- The labor market is no longer running “hot,” yet it is still generating jobs and keeping unemployment within a range historically consistent with expansion rather than contraction.

As we move further into 2026, markets are likely to remain sensitive to incoming data on these three fronts—growth, inflation and employment—as well as to signals from the Federal Reserve about the path of interest rates. January’s modest stock gains alongside steady inflation and slower job growth illustrate how the current environment can support risk assets, even as it demands close attention to the evolving balance of risks.

This market commentary is meant for informational and educational purposes only and does not consider any individual personal considerations. As such, the information contained herein is not intended to be personal investment advice or a recommendation of any kind. The commentary represents an assessment of the market environment through December 2025.

The views and opinions expressed may change based on the market or other conditions. The forward-looking statements are based on certain assumptions, but there can be no assurance that forward-looking statements will materialize.

Equity securities are subject to price fluctuation and investments made in small and mid-cap companies generally involve a higher degree of risk and volatility than investments in large-cap companies. International securities are generally subject to increased risks, including currency fluctuations and social, economic, and political uncertainties, which could increase volatility. These risks are magnified in emerging markets.

Fixed-income securities are subject to loss of principal during periods of rising interest rates and are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications, and other factors. Interest rates and bond prices tend to move in opposite directions. When interest rates fall, bond prices typically rise, and conversely, when interest rates rise, bond prices typically fall.

There is no assurance that any investment, plan, or strategy will be successful. Investing involves risk, including the possible loss of principal. Past performance does not guarantee future results, and nothing herein should be interpreted as an indication of future performance. Please consult your financial professional before making any investment or financial decisions.

AdvicePeriod is another business name and brand utilized by both Mariner, LLC and Mariner Platform Solutions, LLC, each of which is an SEC registered investment adviser. Registration of an investment adviser does not imply a certain level of skill or training. For additional information about Mariner, LLC or Mariner Platform Solutions, LLC, including fees and services, please contact us utilizing the contact information provided herein or refer to the Investment Adviser Public Disclosure website (www.adviserinfo.sec.gov).

For additional information as to which entity your adviser is registered as an investment adviser representative, please refer to the Investment Adviser Public Disclosure website (www.adviserinfo.sec.gov) or the Form ADV 2B provided to you. Investment adviser representatives of Mariner, LLC are generally employees. Investment adviser representatives of Mariner Platform Solutions, LLC dba AdvicePeriod, are independent contractors.

Indexes referenced are unmanaged and cannot be directly invested into. For index definitions visit https://www.marinerwealthadvisors.com/index-definitions/.

Does past performance matter?

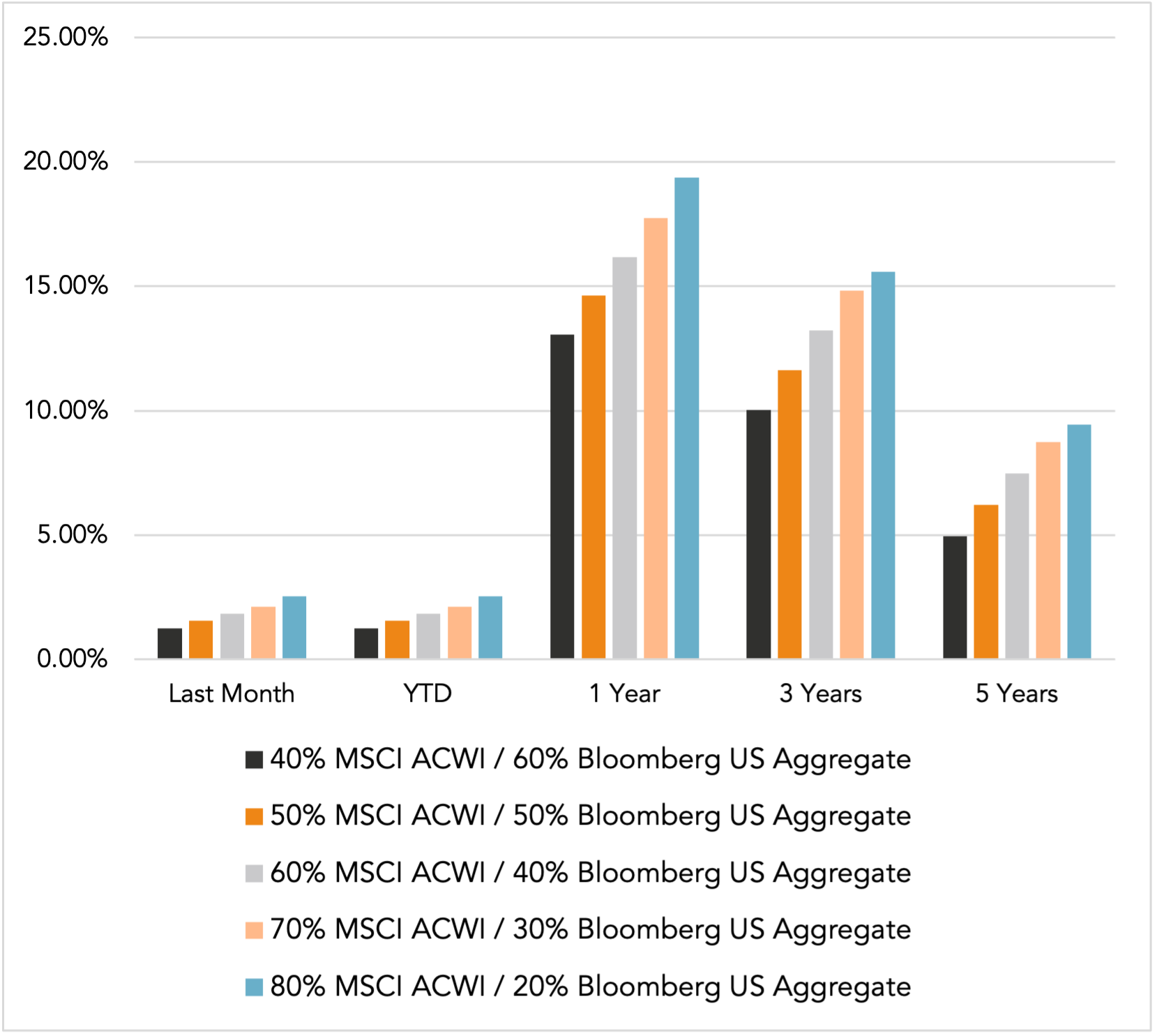

Major Market Index Returns

Period Ending 1/1/2026

Multi-year returns are annualized.

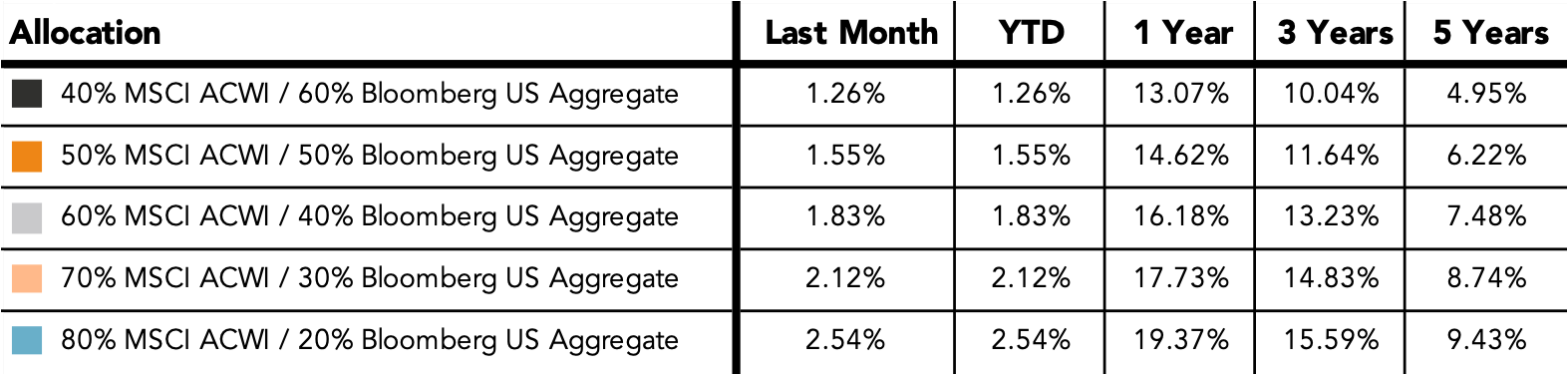

Mix Index Returns

Global Equity / US Taxable Bonds

Indexes are unmanaged and cannot be directly invested into. Past performance is no indication of future results. Investing involves risk and the potential to lose principal.

The Russell 3000 Index is a United States market index that tracks the 3000 largest companies. MSCI Emerging Markets Index is a broad market cap-weighted Index showing the performance of equities across 23 emerging market countries defined as emerging markets by MSCI. MSCI ACWI ex-U.S. Index is a free-float adjusted market capitalization-weighted index that is designed to measure the equity market performance of developed and emerging markets excluding companies based in the United States. Bloomberg U.S. Aggregate Bond Index represents the investment-grade, U.S. dollar-denominated, fixed-rate taxable bond market, including Treasuries, government-related and corporate securities, as well as mortgage and asset-backed securities. Bloomberg Municipal Index is the US Municipal Index that covers the US dollar-denominated long-term tax-exempt bond market. The index has four main sectors: state and local general obligation bonds, revenue bonds, insured bonds, and prerefunded bonds.

Monthly Market Update – February 2026