Please find our most recent market review below. We hope these perspectives are valuable to you.

– The AdvicePeriod Team

Key Observations

- Global growth in 2025 was moderate rather than recessionary, with advanced economies growing modestly and emerging markets expanding faster, keeping world GDP just above 3%. Disinflation, lower energy prices in some regions, and relatively solid labor markets produced a soft‑landing style outcome instead of the deep downturn many had feared.

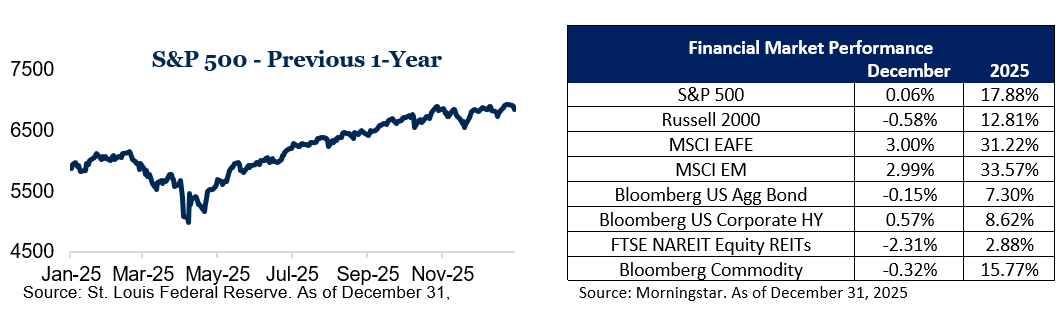

- Broad indices of stocks outside the U.S., such as MSCI ACWI ex USA, returned over 30% in 2025, significantly ahead of the S&P 500’s 17.9% gain. Emerging markets in Asia and Latin America were key drivers, as they outperformed U.S. equities by a wide margin, helped by a weaker dollar and strong local rallies.

- Major central banks shifted from aggressive tightening to the early stages of easing in 2025 as inflation moved closer to targets. This pivot supported rate‑sensitive assets like longer‑duration bonds, real estate and parts of the financial sector, helping sustain equity valuations despite slower growth.

Global markets closed out 2025 on a strong and somewhat surprising note, and December’s data largely reinforced three core themes: the global economy has slowed but remained resilient, international and emerging‑market equities outperformed U.S. stocks, and interest rates appear to have peaked and begun to move lower. These dynamics shaped both portfolio returns and the investment backdrop as we headed into the new year, and they continue to frame the environment for long‑term investors.

Economy: slow but resilient

Despite persistent concerns about recession, the global economy has so far delivered a “slow but resilient” outcome rather than a deep downturn. For 2025, global growth settled into a moderate range, with advanced economies expanding at a modest pace and emerging markets growing faster, leaving world GDP growth just above 3% for the year.

This performance stands in contrast to the more pessimistic forecasts that prevailed at the start of the tightening cycle. Several factors helped cushion the impact of higher interest rates: consumers in many countries still benefited from solid labor markets and wage gains; corporate balance sheets entered the period in relatively healthy shape; and banks, in general, were better capitalized than in prior cycles.

Disinflation has been another crucial element of this story. Headline inflation rates fell significantly from their peaks in most major economies, helped by easing supply‑chain pressures, more stable goods prices and, in some cases, lower or more stable energy prices. While services inflation and wage growth remained somewhat elevated in certain regions, the overall trend gave central banks more confidence that their earlier tightening was gaining traction.

From a regional perspective, growth has not been uniform. Some European economies continued to wrestle with weak industrial activity and the lingering effects of higher energy costs, while parts of Asia, especially in emerging markets, benefited from stronger domestic demand and improving export conditions. In North America, activity cooled but remained supported by consumer spending and ongoing investment in areas such as technology and infrastructure.

The net result is a picture of an economy that has slowed from the rapid post‑pandemic rebound but has, so far, avoided the more severe scenarios that were widely discussed when rate hikes began. As always, risks remain—ranging from geopolitical tensions to policy missteps and financial‑market stress—but the data through year end point to an environment that is challenging yet navigable for diversified investors.

International and EM leadership

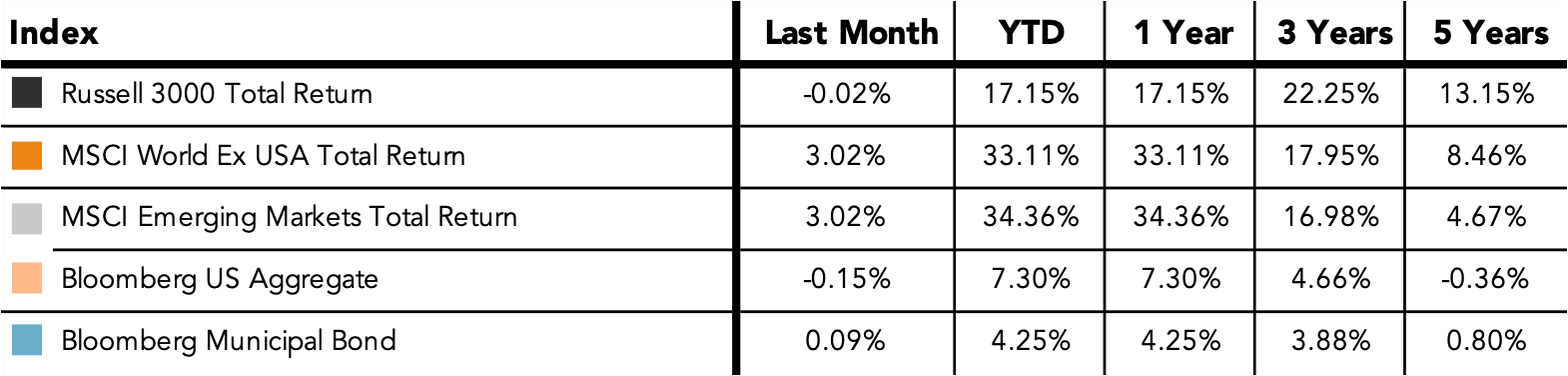

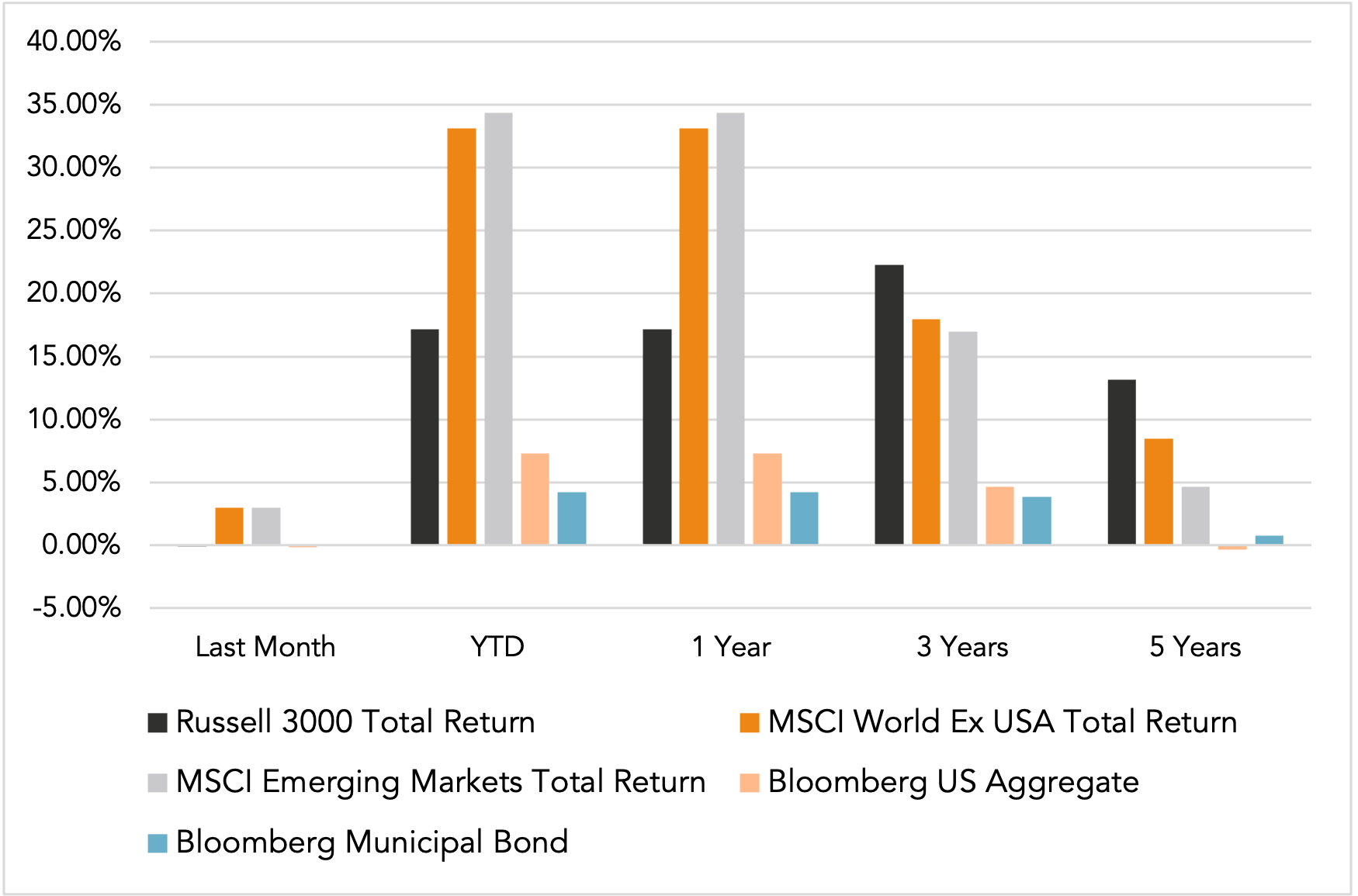

Equity performance over the past year has marked a meaningful shift from the U.S.‑centric leadership that dominated much of the last decade. In 2025, broad indices of stocks outside the U.S., such as MSCI ACWI ex‑USA, delivered returns of 32.4%, outpacing the S&P 500’s 17.9% gain by a significant margin.

Within that broad international universe, emerging markets were especially strong contributors. Markets in Asia and Latin America benefited from a combination of improving growth, cooling inflation and currency strength against the U.S. dollar, which together boosted local‑currency returns when translated back into dollars. Several individual countries posted very strong double‑digit performances, and sector composition—in particular heavier weights to financials, industrials and cyclical value areas—further supported relative returns compared with the more growth‑ and technology‑heavy U.S. market.

This leadership from international and emerging‑market equities reflects a mix of fundamentals and starting valuations. Many non‑U.S. markets entered 2025 trading at discounts to their long‑term averages and at even steeper discounts versus the U.S., leaving more room for both earnings recovery and multiple expansion once macro conditions stabilized. As inflation eased and global growth proved more durable than expected, investors were willing to re‑rate these regions upward, particularly where reforms, improving corporate governance or commodity exposure offered additional support.

For diversified investors, the past year has been a reminder that market leadership is not static and that extended periods of U.S. dominance can be followed by intervals where other regions take the lead. The month’s data and year‑end figures together underscore the ongoing importance of maintaining exposure to a broad global opportunity set rather than relying on any single geography to drive long‑term results.

Interest rates: from peak to easing

A third defining feature of the backdrop has been the shift in interest‑rate dynamics, which continued to play out through the end of the year. After an aggressive tightening cycle that began in 2022, major central banks spent much of 2025 on hold and then, as inflation eased closer to their targets, began to signal and implement the first steps toward rate cuts.

This transition from tightening to early easing has meaningful implications for both bond and equity markets. Longer‑maturity government bonds, which struggled during the sharp rise in yields, saw better performance as markets priced in a plateau and eventual decline in policy rates. Credit markets remained generally well supported, helped by still‑solid corporate balance sheets and the absence, to date, of a deep economic downturn.

On the equity side, sectors and styles that are more sensitive to interest‑rate moves—such as real estate, parts of the financial sector and some growth companies—responded to the prospect of lower discount rates and more stable financing costs. At the same time, the rate backdrop helped sustain overall equity valuations even as profit growth moderated, since lower expected yields on cash and high‑quality bonds can make future stock earnings relatively more attractive.

It is worth noting, however, that central banks have been cautious in their messaging. While inflation has moved meaningfully lower from its peaks, officials have generally emphasized a data‑dependent approach, aiming to avoid cutting too quickly and risking a resurgence of price pressures. As a result, markets have periodically reassessed the pace and depth of potential easing, leading to bouts of volatility in both bond yields and rate‑sensitive sectors.

Taken together, the latest developments suggest that policy rates are likely near, or just past, their cyclical highs in many major economies, but that the path toward more normal levels may be gradual. For investors, this environment continues to reward attention to interest‑rate risk across asset classes and to the interplay between monetary policy, inflation and economic growth.

Putting the month in context

For investor portfolios, December and the year as a whole reinforced several long‑standing themes. Equity markets delivered solid returns, especially outside the U.S., while the inflection in the interest‑rate cycle improved the outlook for fixed income after an extended period of headwinds. The global economy grew more slowly but remained on its feet, supporting corporate earnings and limiting credit stress.

In this type of environment, short‑term market moves can be driven as much by shifting expectations about policy and growth as by the data itself. Monthly updates therefore serve as a way to place those moves in context: the economy has been slow but resilient, international and emerging markets have recently led performance, and rates appear to be transitioning from headwind to potential tailwind. These broad patterns, rather than any single month’s volatility, are what ultimately matter most for long‑term investors.

Thank you for your trust, and happy New Year!

This market commentary is meant for informational and educational purposes only and does not consider any individual personal considerations. As such, the information contained herein is not intended to be personal investment advice or a recommendation of any kind. The commentary represents an assessment of the market environment through December 2025.

The views and opinions expressed may change based on the market or other conditions. The forward-looking statements are based on certain assumptions, but there can be no assurance that forward-looking statements will materialize.

Equity securities are subject to price fluctuation and investments made in small and mid-cap companies generally involve a higher degree of risk and volatility than investments in large-cap companies. International securities are generally subject to increased risks, including currency fluctuations and social, economic, and political uncertainties, which could increase volatility. These risks are magnified in emerging markets.

Fixed-income securities are subject to loss of principal during periods of rising interest rates and are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications, and other factors. Interest rates and bond prices tend to move in opposite directions. When interest rates fall, bond prices typically rise, and conversely, when interest rates rise, bond prices typically fall.

There is no assurance that any investment, plan, or strategy will be successful. Investing involves risk, including the possible loss of principal. Past performance does not guarantee future results, and nothing herein should be interpreted as an indication of future performance. Please consult your financial professional before making any investment or financial decisions.

AdvicePeriod is another business name and brand utilized by both Mariner, LLC and Mariner Platform Solutions, LLC, each of which is an SEC registered investment adviser. Registration of an investment adviser does not imply a certain level of skill or training. For additional information about Mariner, LLC or Mariner Platform Solutions, LLC, including fees and services, please contact us utilizing the contact information provided herein or refer to the Investment Adviser Public Disclosure website (www.adviserinfo.sec.gov).

For additional information as to which entity your adviser is registered as an investment adviser representative, please refer to the Investment Adviser Public Disclosure website (www.adviserinfo.sec.gov) or the Form ADV 2B provided to you. Investment adviser representatives of Mariner, LLC are generally employees. Investment adviser representatives of Mariner Platform Solutions, LLC dba AdvicePeriod, are independent contractors.

Indexes referenced are unmanaged and cannot be directly invested into. For index definitions visit https://www.marinerwealthadvisors.com/index-definitions/.

Does past performance matter?

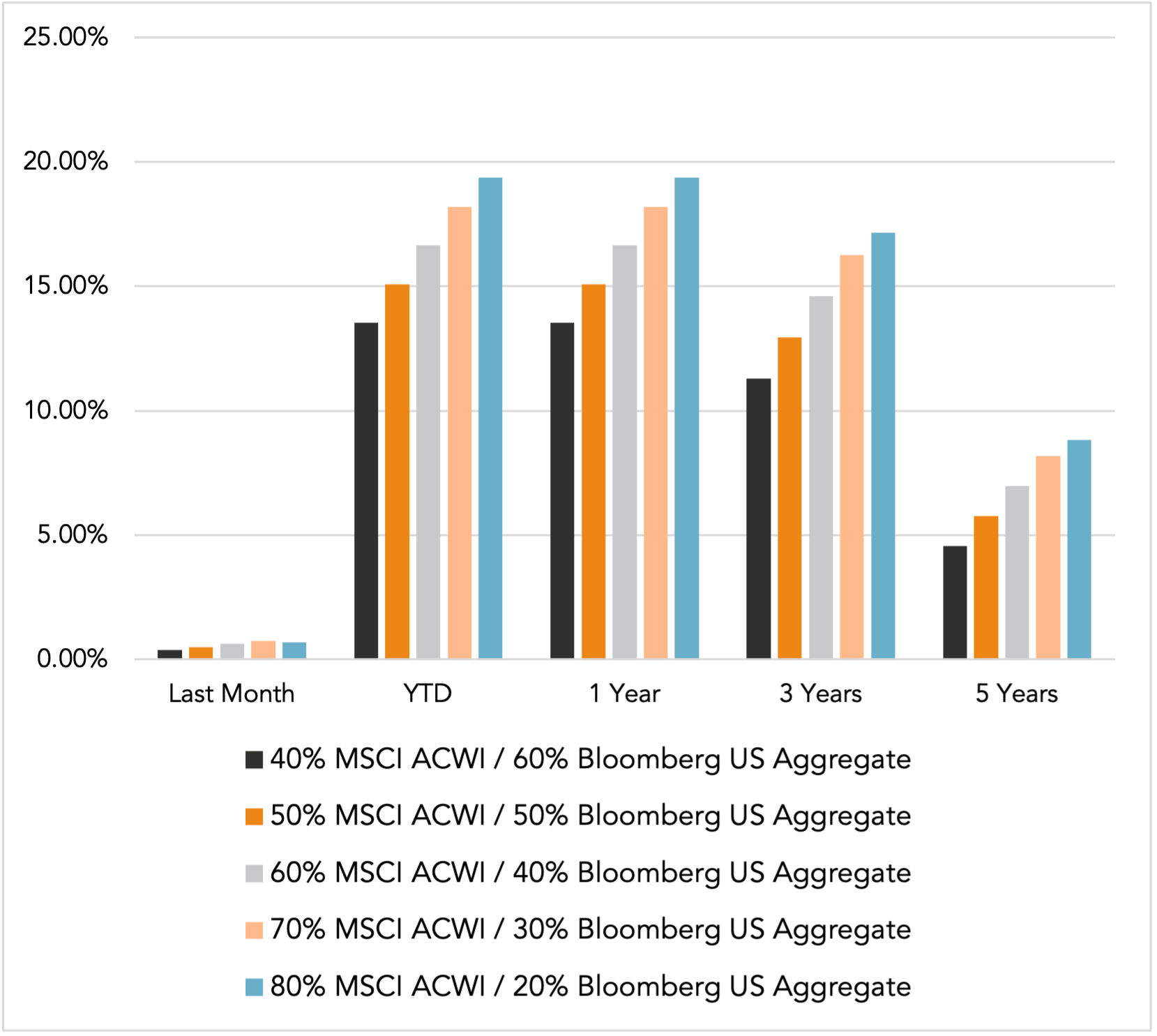

Major Market Index Returns

Period Ending 12/1/2025

Multi-year returns are annualized.

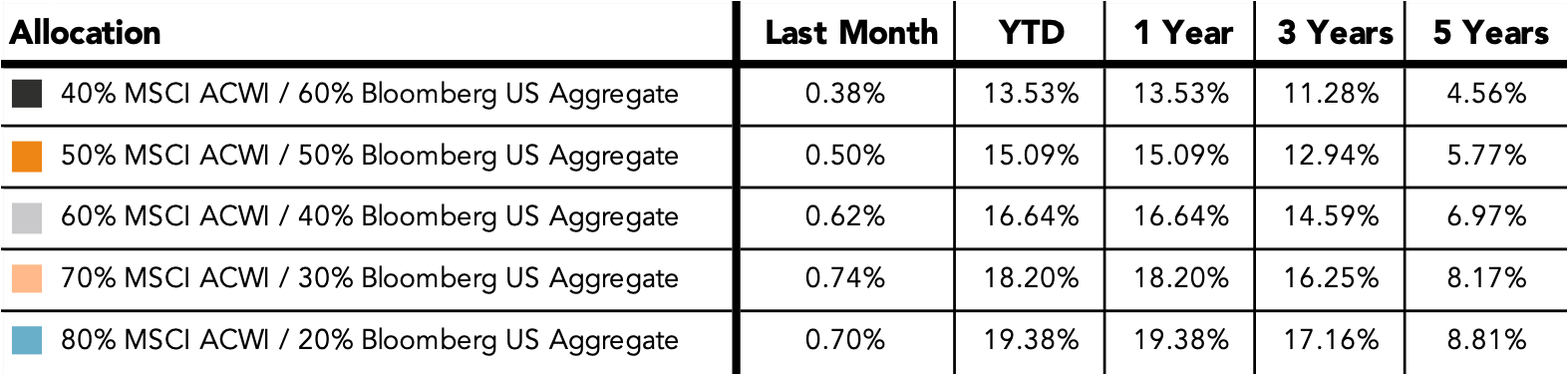

Mix Index Returns

Global Equity / US Taxable Bonds

Indexes are unmanaged and cannot be directly invested into. Past performance is no indication of future results. Investing involves risk and the potential to lose principal.

The Russell 3000 Index is a United States market index that tracks the 3000 largest companies. MSCI Emerging Markets Index is a broad market cap-weighted Index showing the performance of equities across 23 emerging market countries defined as emerging markets by MSCI. MSCI ACWI ex-U.S. Index is a free-float adjusted market capitalization-weighted index that is designed to measure the equity market performance of developed and emerging markets excluding companies based in the United States. Bloomberg U.S. Aggregate Bond Index represents the investment-grade, U.S. dollar-denominated, fixed-rate taxable bond market, including Treasuries, government-related and corporate securities, as well as mortgage and asset-backed securities. Bloomberg Municipal Index is the US Municipal Index that covers the US dollar-denominated long-term tax-exempt bond market. The index has four main sectors: state and local general obligation bonds, revenue bonds, insured bonds, and prerefunded bonds.

Monthly Market Update – January 2026