Please find our most recent market review below. We hope these perspectives are valuable to you.

– The AdvicePeriod Team

The Recession Will Have to Wait

The global economy continued to grow through the first four months of the year. Bonds continued to move higher, and international stocks outperformed U.S. equities. Meanwhile, investors continue to anticipate an end to the Federal Reserve’s rate-hiking cycle.

Key Observations

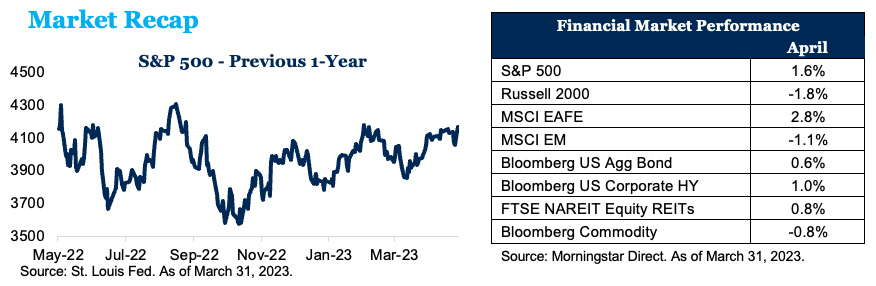

- The stock market was slightly higher in April.

- Small-cap stocks declined due to economic concerns.

- Bonds ended the month moderately higher.

- International developed markets posted a healthy gain, but emerging markets fell.

- Chinese stocks lost 5.2% for the month.

The stock market held its own in April despite downbeat economic data, worries about the banking sector and weaker earnings. Bonds continued to rally in anticipation of the end of the Federal Reserve’s rate-hiking cycle in the coming months. While the S&P 500 is up 14.7% from its bear-market low on Oct. 14, the market is only 6.1% higher than it was at the end of November. The Bloomberg U.S. Aggregate Bond Index gained 0.6% for the month, while yields stayed relative flat: 2-year Treasury yields, which began the month at 4.04%, dropped to 4.02%, and the 10-year Treasury yield rose from 3.34% to 3.43%. Small- and mid-cap stocks fell 1.8% and 0.5%, respectively. International markets ended the month with moderate gains, outperforming the U.S. market as the U.S. dollar declined.

Q1 gross domestic product rose at a 1.1% annualized rate, lagging analyst expectations. Major drivers were declines in business investment and in inventories as companies continue to be weighed down by the Fed’s interest-rate hikes. Despite a decline in business investment, consumer spending continues to surge as the consumer has benefited from low unemployment and steady wage gains. Given the strength of the consumer and core CPI continuing to stay higher longer than hoped, it is likely the Fed will continue its hiking path in May. If the Federal Open Market Committee votes for another 25-basis-point hike in the federal funds rate at the May 2-3 meeting, Fed Chair Jerome Powell is likely to announce a pause in additional hikes for the time being.

Recession or Soft Landing?

The Index of Leading Economic Indicators (LEI) peaked at a record high in February 2022 and has been falling ever since. Existing home sales dropped 2.4% during March after surging 14.5% in February. A shortage of homes for sale is frustrating home buyers but keeping homes prices firm. Initial claims for state unemployment benefits rose 5,000 to a seasonally adjusted 245,000 for the week ended April 15. That low level of jobless claims shows that jobs remain plentiful. The Fed’s latest Beige Book report described job gains as having “moderated somewhat” in early April “as several districts reported a slower pace of growth” than in recent months. The report also noted that banks had tightened lending standards because of the recent collapse of Silicon Valley Bank, Signature Bank and Credit Suisse. These reports together show an economy that is slowing but is not collapsing, providing hope to those still expecting a soft landing.

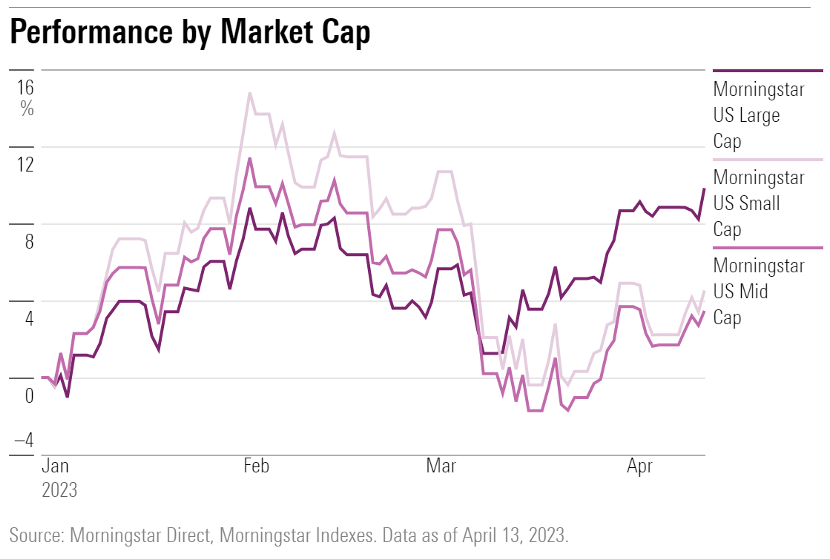

Large-Cap Surge

The Morningstar US Large Cap Index—which measures the performance of the largest 70% capitalization of U.S. large-cap stocks—gained 9.8% for the year through April 13, while the broader market gained 9.2% as measured by the Morningstar US Market Index. For the same period, small-cap stocks rose only 4.5% as measured by the Morningstar US Small Cap Index. Among sectors, technology and communication stocks have led the latest surge in large caps. The drop in interest rates has been a big driver of growth stocks in the large-cap index. The Morningstar US Large Growth Index gained 17.8% for the same period. That’s a reversal from last year when large-cap stocks lost 20.4% as a group, led by large growth, which fell 40.4% last year. With such dramatic swings in performance, it is important that investors maintain good balance in their portfolios regarding style and size.

Outlook

At the beginning of last year, the consensus view was that inflationary pressures were transitory. Then, as inflation began to surge, the Fed embarked on one of the most aggressive series of rate hikes in its history, and the consensus view was that an economic recession would surely follow. Now, with inflation slowly moderating and stock and bond prices rallying, the experts have changed their view once again and seem to believe a “soft landing” in the economy is achievable. We believe this constant flip-flopping of views is just the latest example of why investors should stay the course and stay focused on their long-term financial goals and pay little attention to the predictions and prognostications of the “experts.”

Disclosures:

This market commentary is meant for informational and educational purposes only and does not consider any individual personal considerations. As such, the information contained herein is not intended to be personal investment advice or recommendation. Please consult a financial professional before making any financial-related decisions.

The commentary represents an assessment of the market environment through April 2023. The views and opinions expressed may change based on the market or other conditions. The forward-looking statements are based on certain assumptions, but there can be no assurance that forward-looking statements will materialize. This commentary was written and provided by an unaffiliated third party.

Indexes are unmanaged and cannot be directly invested into. Past performance is no indication of future results. Investing involves risk and the potential to lose principal.

AdvicePeriod is another business name and brand utilized by both Mariner, LLC and Mariner Platform Solutions, LLC, each of which is an SEC registered investment adviser. Registration of an investment adviser does not imply a certain level of skill or training. Each firm is in compliance with the current notice filing requirements imposed upon SEC registered investment advisers by those states in which each firm maintains clients. Each firm may only transact business in those states in which it is notice filed or qualifies for an exemption or exclusion from notice filing requirements. Any subsequent, direct communication by an advisor with a prospective client shall be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides. For additional information about Mariner, LLC or Mariner Platform Solutions, LLC, including fees and services, please contact us utilizing the contact information provided herein or refer to the Investment Adviser Public Disclosure website (www.adviserinfo.sec.gov). Please read the disclosure statement carefully before you invest or send money.

For additional information as to which entity your adviser is registered as an investment adviser representative, please refer to the Investment Adviser Public Disclosure website (www.adviserinfo.sec.gov) or the Form ADV 2B provided to you. Investment adviser representatives of Mariner, LLC dba Mariner Wealth Advisors and dba AdvicePeriod are generally employed by Mariner Wealth Advisors, LLC. Investment adviser representatives of Mariner Platform Solutions, LLC dba AdvicePeriod, are independent contractors.

Index Definitions: The S&P 500 is a capitalization-weighted index designed to measure the performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries. Russell 2000 consists of the 2,000 smallest U.S. companies in the Russell 3000 index. MSCI EAFE is an equity index which captures large and mid-cap representation across Developed Markets countries around the world, excluding the U.S. and Canada. The index covers approximately 85% of the free float-adjusted market capitalization in each country. MSCI Emerging Markets captures large and mid-cap representation across Emerging Markets countries. The index covers approximately 85% of the free-float adjusted market capitalization in each country. Bloomberg U.S. Aggregate Index covers the U.S. investment grade fixed rate bond market, with index components for government and corporate securities, mortgage pass-through securities, and asset-backed securities. Bloomberg U.S. Corporate High Yield Index covers the universe of fixed rate, non-investment grade debt. Eurobonds and debt issues from countries designated as emerging markets (sovereign rating of Baa1/BBB+/BBB+ and below using the middle of Moody’s, S&P, and Fitch) are excluded, but Canadian and global bonds (SEC registered) of issuers in non-EMG countries are included. FTSE NAREIT Equity REITs Index contains all Equity REITs not designed as Timber REITs or Infrastructure REITs. Bloomberg Commodity Index is calculated on an excess return basis and reflects commodity futures price movements. The index rebalances annually weighted 2/3 by trading volume, and 1/3 by world production and weight-caps are applied at the commodity, sector, and group level for diversification. Morningstar US Market Index measures the performance of US securities and targets 97% market capitalization coverage of the investable universe. Morningstar US Small Cap Index measures the performance of US small-cap stocks. These stocks fall between the 90th and 97th percentile in market capitalization of the investable universe. In aggregate, the Small Cap Index represents 7 percent of the investable universe. Morningstar US Mid Cap Index measures the performance of US mid-cap stocks. These stocks fall between the 70th and 90th percentile in market capitalization of the investable universe. In aggregate, the Mid-Cap Index represents 20 percent of the investable universe. Morningstar US Large Growth Index is designed to provide consistent representation of the large-cap growth segment of the US equity market, with no overlapping constituents across styles.

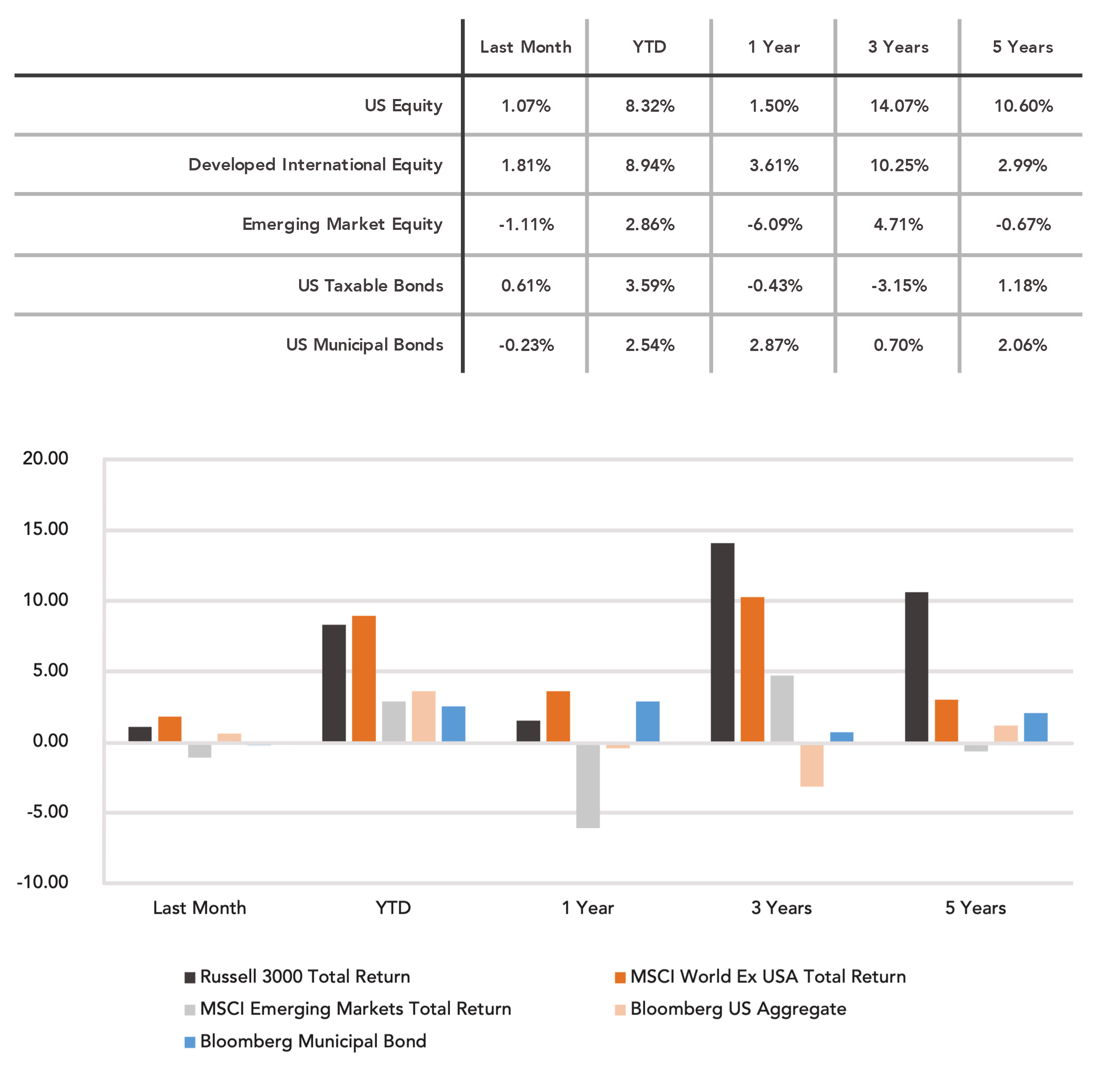

Does past performance matter?

Major Market Index Returns

Period Ending 5/1/2023

Multi-year returns are annualized.

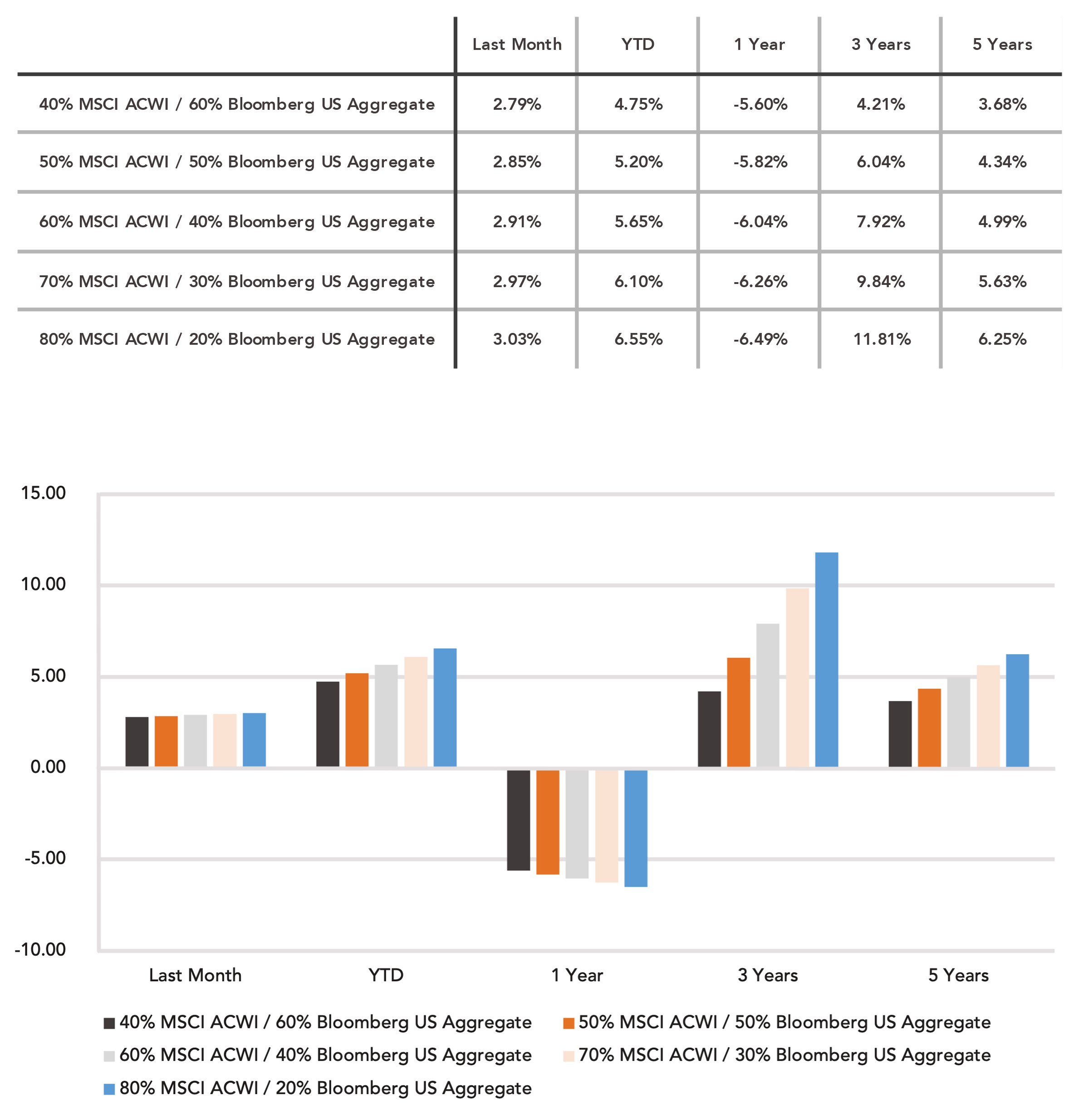

Mix Index Returns

Global Equity / US Taxable Bonds

Indexes are unmanaged and cannot be directly invested into. Past performance is no indication of future results. Investing involves risk and the potential to lose principal.

The Russell 3000 Index is a United States market index that tracks the 3000 largest companies. MSCI Emerging Markets Index is a broad market cap-weighted Index showing the performance of equities across 23 emerging market countries defined as emerging markets by MSCI. MSCI ACWI ex-U.S. Index is a free-float adjusted market capitalization-weighted index that is designed to measure the equity market performance of developed and emerging markets excluding companies based in the United States. Bloomberg U.S. Aggregate Bond Index represents the investment-grade, U.S. dollar-denominated, fixed-rate taxable bond market, including Treasuries, government-related and corporate securities, as well as mortgage and asset-backed securities. Bloomberg Municipal Index is the US Municipal Index that covers the US dollar-denominated long-term tax-exempt bond market. The index has four main sectors: state and local general obligation bonds, revenue bonds, insured bonds, and prerefunded bonds.

April 2024 Market Commentary